6/21 Weekly Analysis - A Week Divided by the Fed's Hawkish Hold, Oil Price Plunge, and Divergence Between Energy Decline and Consumer/Financial Recovery

June 21, 2026 Weekly Market Analysis

## This Week's Key Theme: Fed's Hawkish Hold + Oil Price Plunge, Shift of Momentum from Energy to Consumer

This week (June 15-21, US Eastern Time), the US stock market had two major themes.

1. The Fed's 'Hawkish Hold'

- On June 17, the Federal Open Market Committee (FOMC) held the policy rate at 3.50-3.75%, but through the dot plot and commentary strongly signaled the possibility of additional rate increases within the year.(stocktitan.net)

- With inflation forecasts (PCE, including core PCE) revised upward, the market interpreted this as a signal that "while rates were not raised immediately, the direction has shifted toward increases rather than decreases."(stocktitan.net)

- This weighed on highly valued growth stocks and tech stocks, while acting as a relative tailwind for dividend stocks with economic resilience, essential consumer staples, and financials.

2. Expectations for US-Iran Ceasefire and Crude Oil Transport Resumption → Oil Price Plunge → Energy Weakness + Fuel Cost Beneficiary Strength

- Following news that the US and Iran provisionally agreed on a war-related ceasefire and reopening of the Strait of Hormuz, Brent crude fell 4.8% early this week to drop below $80, with further declines below $80 thereafter.(apnews.com)

- While the oil price decline is a headwind for energy company profit prospects, it acted as a cost reduction factor for sectors with high fuel cost exposure such as airlines, transportation, and consumer-related industries.

In summary, in a somewhat ironic environment where "inflation pressure remains high but energy prices are plummeting," the energy sector was significantly pressured while consumer, financial, and cyclical stocks gained momentum this week.

---

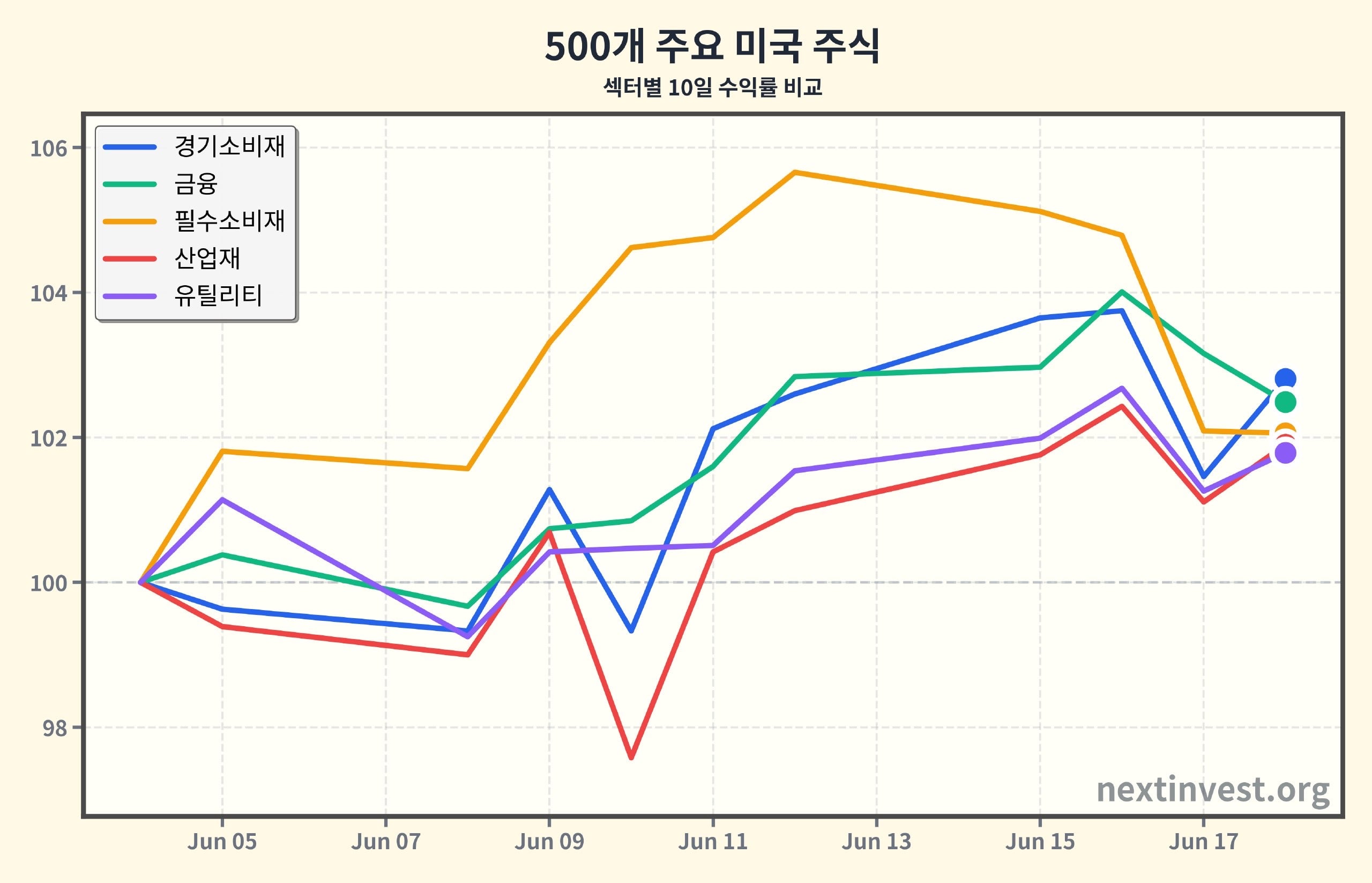

## Sector Performance: 10-Day (10D) Basis, Energy and Communication Weakness vs. Consumer, Financial, and Cyclical Strength

### 1) Overall Picture

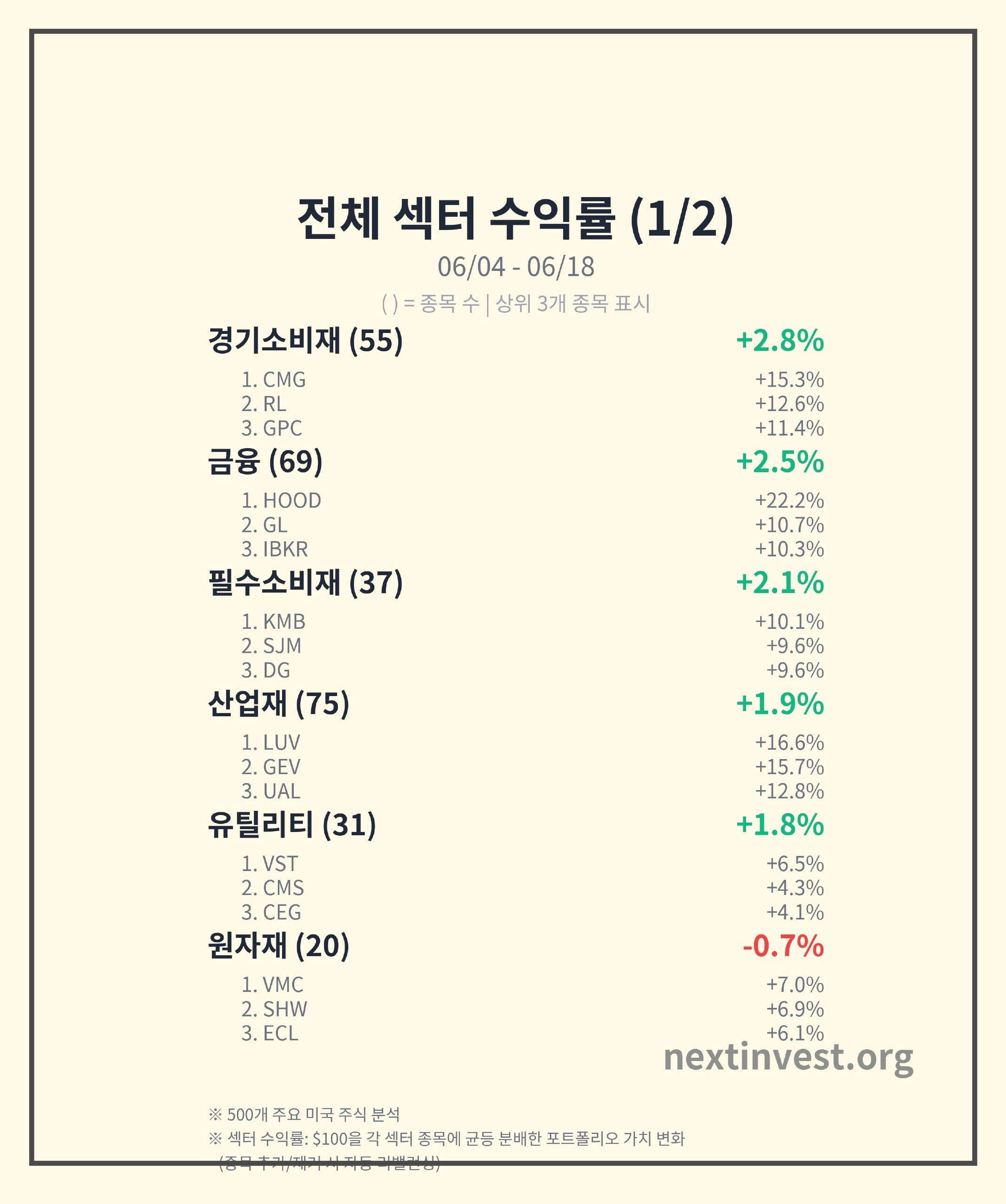

- Of 11 sectors on a 10-day (10D) performance basis, 5 are up.

- Best: Consumer Cyclical (+2.81%)

- Worst: Energy (-8.67%)

- Looking at 30-day and 120-day trends,

- Technology (Tech): Despite a 10D -4.72% short-term correction, it remains the medium to long-term leader at 30D +9.46%, 120D +42.25%.

- Communication Services: 10D -3.90%, 30D -6.99%, 120D -10.37%, a period of continued medium to long-term weakness.

- Energy: 10D -8.67%, 30D -6.30%, but 120D +23.81%, appearing to enter a fatigue and correction phase after a long-term rally.

Additionally, looking at sector trends on approximately a 60 trading day basis (pipeline analysis):

- Technology: +33.3% total gain since end of March, maintaining a gradual uptrend (+3.33%) from June 5 onward.

- Energy: Continuing a downtrend of approximately -10.9% from May 18 to present.

- Communication Services: -7.35% decline from June 1, with -10% range underperformance on a 120-day basis.

In other words, this week's 10D movement is not mere short-term noise, but rather flows that are to some extent aligned with already-established medium to long-term trends (tech strength and fatigue in energy and some defensive sectors).

---

## In-Depth Sector Commentary

### Consumer Cyclical – Benefiting from Oil Price Decline + Leisure/Dining Consumption Recovery

- 10D Return: +2.81% (1st of 11)

- Representative Stocks: Chipotle (CMG, +15.29%), Ralph Lauren (RL, +12.62%), Genuine Parts (GPC, +11.41%)

What happened?

1. Oil Price Plunge → Cost Burden Relief for Consumer and Leisure Sectors

- Crude oil prices fell below $80 a barrel (apnews.com) amid expectations of a ceasefire in Iran and the reopening of the Strait of Hormuz, reducing fuel and logistics costs for industries.

- Industries such as airlines, restaurants, and distribution saw even small increases in revenue translate into significant cost leverage, with the market quickly reflecting this in stock prices.

2. Expectations for Consumer Spending Recovery

- Although the Fed froze interest rates while strongly mentioning inflation (washingtonpost.com), the fact that it did not raise rates immediately somewhat eased concerns about a slowdown in consumption.

- The interpretation that "prices are high, but consumption has not yet significantly declined" is reflected in mid-to-high-end brands (e.g., Ralph Lauren) and high-margin restaurants (Chipotle).

What it Means to Me

- In the short term, the formula that "falling oil prices = a favorable environment for travel, dining, and shopping" is working again.

- However, with cyclical consumer goods at -3.35% based on a 120D standard, it's still in the long-term adjustment zone. Compared to long-term structurally growing stocks (such as tech), it's important to remember that this is a "mood genre" sector with high volatility.

---

### Financial Services – Rebound on Signal that "Interest Rates May Rise Further"

- 10D Return: +2.49% (2nd)

- Representative Stocks: Robinhood(HOOD, +22.16%), Globe Life(GL, +10.66%), Interactive Brokers(IBKR, +10.27%)

Key Background

1. Fed's Hawkish Freeze → Long-Term Interest Rates and Margin Expectations Rise

- The dot plot showed a signal that interest rates could be higher than the current level by the end of 2026 (stocktitan.net), and

- This acted as a positive factor for banks, insurance companies, and other financial institutions that generate revenue through deposit-loan spreads.

- While the 30D financial sector was +2.82% and the 120D sector was -1.54%, it is still difficult to say that a long-term reversal has occurred. However, the recent 10D rebound can be interpreted as an attempt to "bottom out."

2. Trading and Investment Platform Benefits

- Increased volatility led to expectations of increased brokerage fees and trading commissions for platforms like Robinhood and Interactive Brokers.

Investor Perspective

- Mixing a portion of the financial sector into a portfolio centered on high-growth tech stocks can

- Act as a hedge (buffer) when inflation and interest rate upside risks increase.

- However, since it is still uncertain whether the Fed will actually raise rates or just apply pressure verbally, "a gradual diversification into interest rate-sensitive sectors" is a realistic approach.

---

### Consumer Defensive – Steady Plus, but Trends are Shaky

- 10D Return: +2.06%

- Representative Stocks: Kimberly-Clark(KMB, +10.05%), J.M. Smucker(SJM, +9.63%), Dollar General(DG, +9.59%)

- Consumer staples and discount retailers are industries that generate stable cash flow based on consistent demand even under price pressure.

- As the Fed continues to emphasize inflation while maintaining a stance against recession (unboxfuture.com),

- The structure of "continued living expense burden → consumer patterns shifting towards low prices and PB" is being confirmed again.

However, looking at the 60-trading day trend:

- The consumer defensive sector has been in a downward phase of -3.43% since June 12th, so it is still too early to say that the 10D rebound represents a bullish trend.

Meaning for Daily Life

- The fact that consumer defensive stock prices are resilient means

- This means people "continue buying daily necessities and low-cost food even while cutting back on dining out/travel," and

- at the same time, it is a signal that real cost-of-living pressures have not yet ended.

---

### Industrials and Utilities – Additional Beneficiaries of Falling Oil Prices

- Industrials 10D: +1.90%

- Top beneficiaries: Southwest(LUV, +16.63%), GE Vernova(GEV, +15.70%), United Airlines(UAL, +12.75%)

- Utilities 10D: +1.79%

- Top beneficiaries: Vistra(VST, +6.54%), CMS Energy(CMS, +4.29%), Constellation Energy(CEG, +4.12%)

Why are they rising together?

1. Airlines/Transportation: Falling oil prices = direct profit

- Because fuel costs make up a very large share of airlines' cost structure, even a few percent drop in oil prices significantly improves operating margins.(apnews.com)

- This is the backdrop behind airline stocks like LUV and UAL delivering double-digit gains.

2. Utilities: Rate fatigue + defensive stock preference

- With interest rates on hold and bond yields not surging sharply(stocktitan.net), the power and public utility sector — less sensitive to the economic cycle and energy prices — has been re-rated as a defensive play.

- With 120D performance also at +7.28%, utilities have been playing the classic alternative asset role of "dividend + defense" so far this year.

---

### Technology – 10D Pullback, but 120D Leadership Remains

- 10D return: -4.72% (bottom tier)

- 30D: +9.46%, 120D: +42.25% (No. 1 across all sectors)

- Top gainers: Western Digital(WDC, +30.46%), Sandisk(SNDK, +25.19%), Applied Materials(AMAT, +23.00%)

- Top decliners: Super Micro Computer(SMCI, -34.55%), Accenture(ACN, -28.45%), Adobe(ADBE, -24.42%)

What triggered the pullback?

1. Fed's hawkish hold → valuation pressure on high-multiple growth stocks

- As the possibility of rate hikes resurfaced, the discount rate applied to AI, cloud, and software companies with large future earnings expectations moved higher.(stocktitan.net)

2. Stock-specific issues – SMCI's sharp drop

- Super Micro Computer(SMCI) fell roughly 30% in a single week following the announcement of a dilutive $7B capital raise plan and a string of reports on litigation and regulatory risks.(simplywall.st)

- Having already surged significantly as an AI server beneficiary, there was also considerable fatigue around the sense that "most of the good news is already priced in."

3. Storage and semiconductors shining amid the turbulence

- Western Digital(WDC) surged more than 30% in a week on expectations for AI data storage demand, combined with analyst target price upgrades and the company's capital structure disclosures.(quiverquant.com)

- This is read as a signal that "the AI theme is expanding beyond simple GPUs into the surrounding ecosystem of memory, storage, and network infrastructure."

Trends and Implications

- On the 60-trading-day trend, the technology sector surged +33.3% since late March, and after a brief pullback in early June, has been in a gradual uptrend again from June 5.

- The current 10D pullback looks more like "a breather after overheating" rather than a break in the medium-to-long-term growth story —

- it is more appropriate to view this as entering a quality phase where stock selection and valuation discipline become increasingly important.

---

### Communication Services – Sector Continues to Struggle

- 10D: -3.90%

- 30D: -6.99%, 120D: -10.37%

- Leading Performers: Take-Two(TTWO, +10.45%), Live Nation(LYV, +6.35%), Disney(DIS, +3.79%)

While some gaming, entertainment, and content stocks have been buoyed by strong earnings and momentum, the sector as a whole continues to face structural headwinds such as slowing advertising revenue and regulatory risks.

The downward trend that began on June 1st (-7.35%) persists, suggesting that even with short-term rebounds, a cautious, stock-specific approach is still necessary.

---

### Energy – Oil Price Plunge Hits Sector Hard, 120D Rally Followed by Major Correction

- 10D: -8.67% (Lowest among 11 sectors)

- 30D: -6.30%, 120D: +23.81%

- Leading Stocks: Williams(WMB, +1.70%), Kinder Morgan(KMI, -0.35%), Targa(TRGP, -3.29%)

The Link Between Oil Prices and Stock Performance

1. Direct Impact of Oil Price Drop

- Following news of a truce with Iran and the reopening of straits, concerns about supply disruptions eased, leading to a 4.8% drop in Brent crude prices early this week. Prices subsequently fell below $80 per barrel (apnews.com).

- Energy company profits are fundamentally determined by oil prices multiplied by production volume, so the price drop directly translates into reduced profit expectations.

2. Fatigue After Previous Gains

- The energy sector had already seen a significant rise of +23.81% over the past 120 days, largely reflecting anticipated gains from the war and supply concerns.

- With a 10.9% decline in the 60-day trend since May 18th, this week's drop can be interpreted as a combination of technical adjustment and fundamental reassessment.

Consumer and Investment Perspectives

- In the short term, consumers may benefit from a slight decrease in energy costs such as gasoline and heating bills.

- For investors, while the energy sector still holds long-term upside potential, this week served as a reminder that it is highly sensitive to geopolitical variables and can be a volatile "rollercoaster" sector.

---

## Key Stock Trends: Extreme Volatility in AI and Tech

### 1) Super Micro Computer(SMCI) – Dilution Concerns and Legal Risks Trigger 30% Plunge

- A 34.55% drop this week, the worst performance in the sector.

- Investor sentiment soured significantly following the announcement of a $7 billion dilutive capital raise plan and the resurgence of accounting and disclosure lawsuits against the company (simplywall.st).

- This case exemplifies the "overheating followed by exhaustion" phenomenon in a dramatic fashion, as SMCI was previously one of the hottest AI server beneficiaries.

### 2) Western Digital(WDC), Sandisk(SNDK), Applied Materials(AMAT) – Expanding Benefits from AI Infrastructure

- WDC: +30.46%, SNDK: +25.19%, AMAT: +23.00%

- Analyst target price increases and growing anticipation of increased data storage and memory demand in the AI era fueled a substantial rise in WDC (quiverquant.com).

- Semiconductor and equipment companies like AMAT are benefiting from the expanding AI investment cycle, which is expected to extend beyond GPUs to encompass memory, storage, and equipment.

Investment Takeaway

- This week highlighted the stark differences in performance within the AI theme, depending on "what a company sells" and "how expensively it is traded."

- It underscored the importance of considering valuation, regulatory/legal risks, and demand sustainability alongside short-term momentum.

---

## Next Week's Focus Points: "Post-Fed" and "Oil Price Rebound Prospects"

1. First Week After Fed – Market Digestion of Hawkish Messages

- Instead of a "surprise hike," a hawkish hold with verbal pressure came this week.

- Next week, style rotation between bond yields and growth vs. value stocks could deepen further.

- Key Points:

- Whether tech and growth stock corrections will continue,

- Or whether capital flows to financials, value stocks, and dividend stocks will intensify further.

2. Oil Price Direction – Real Supply Normalization or Short-term Event?

- Depending on how sustainable the US-Iran agreement actually is, oil prices will take either a path of further decline or a reversal bounce.(apnews.com)

- If oil prices fall further:

- Burden on energy sector,

- Additional tailwinds for airlines, transportation, and consumer sectors.

- Conversely, if oil prices rebound, the energy sector that plummeted this week could see technical recovery opportunities.

3. Real Economic Data and Inflation Re-confirmation

- The Fed has already emphasized energy-driven inflation risks.(unboxfuture.com)

- If upcoming consumer, employment, and inflation data actually support this,

- Markets may need to endure a state of "pause but effectively tightening" for longer.

---

## Conclusion: Practical Points at This Stage

1. Review All-in Tech Positioning

- On a 120D basis, the tech sector remains an overwhelming leader at +42%.

- However, it showed that when rates, regulation, and stock-specific issues overlap like this week, correction magnitudes can be very large.

- Now is the time to recheck your entire portfolio's sector and style diversification.

2. Energy: Planned Allocation Adjustments, Not Chasing

- Given sensitivity to war and political events, while a reasonable energy allocation as a long-term theme is justified, chasing purchases swept up by short-term news should be avoided.

3. Balance Between Cost of Living and Investing

- Oil price stability is certainly good news in terms of easing cost-of-living pressures.

- At the same time, inflation and rates remain at elevated levels, making cash flow management and emergency fund securing important.

In one sentence, we've entered "a phase where the long-term growth story centered on AI and tech remains valid, but we must fine-tune sector, stock, and rate environment adjustments on top of it." Next week, energy prices and post-Fed bond market reactions are likely to determine the overall tone of the stock market.

This content is written for informational purposes only and does not recommend investment in any specific stocks or assets.

Source: https://nextinvest.org/ko

Free to share without permission ^^