July 1st Week Weekly Market - Employment Slowdown and Sector Rotation: Healthcare & Defensive Stocks Up, High-Valuation Tech & Semiconductors Take a Breather

## This Week's Key Theme: "Interest Rates Won't Rise"… Money Moved to Defensive Stocks

With Independence Day on July 4th shortening the trading week, the US stock market in the first week of July can be summarized as "Employment Slowdown → Interest Rate Freeze Expectations → Sector Rotation."

- As June non-farm employment indicators came out weaker than expected, the market began to lean towards the view that "the Fed will be hesitant to raise rates further." (ethivo-briefing.com)

- As a result, some funds were withdrawn from high-growth tech and semiconductor stocks with expensive valuations, and moved to defensive and dividend sectors (healthcare, consumer staples, finance, utilities) with stable cash flows. (ethivo-briefing.com)

- While the Dow, S&P, and Nasdaq all showed weekly gains, there were different stories unfolding beneath the surface. The Dow hit a record high thanks to its weighting towards cyclical and traditional industry stocks, while the Nasdaq underperformed relatively due to selling pressure on semiconductors and high-valuation growth stocks. (kucoin.com)

What this means for you is simple.

> While interest rate concerns have eased somewhat, the market is signaling a shift from "too expensive growth stocks" to "cash-generating defensive stocks."

---

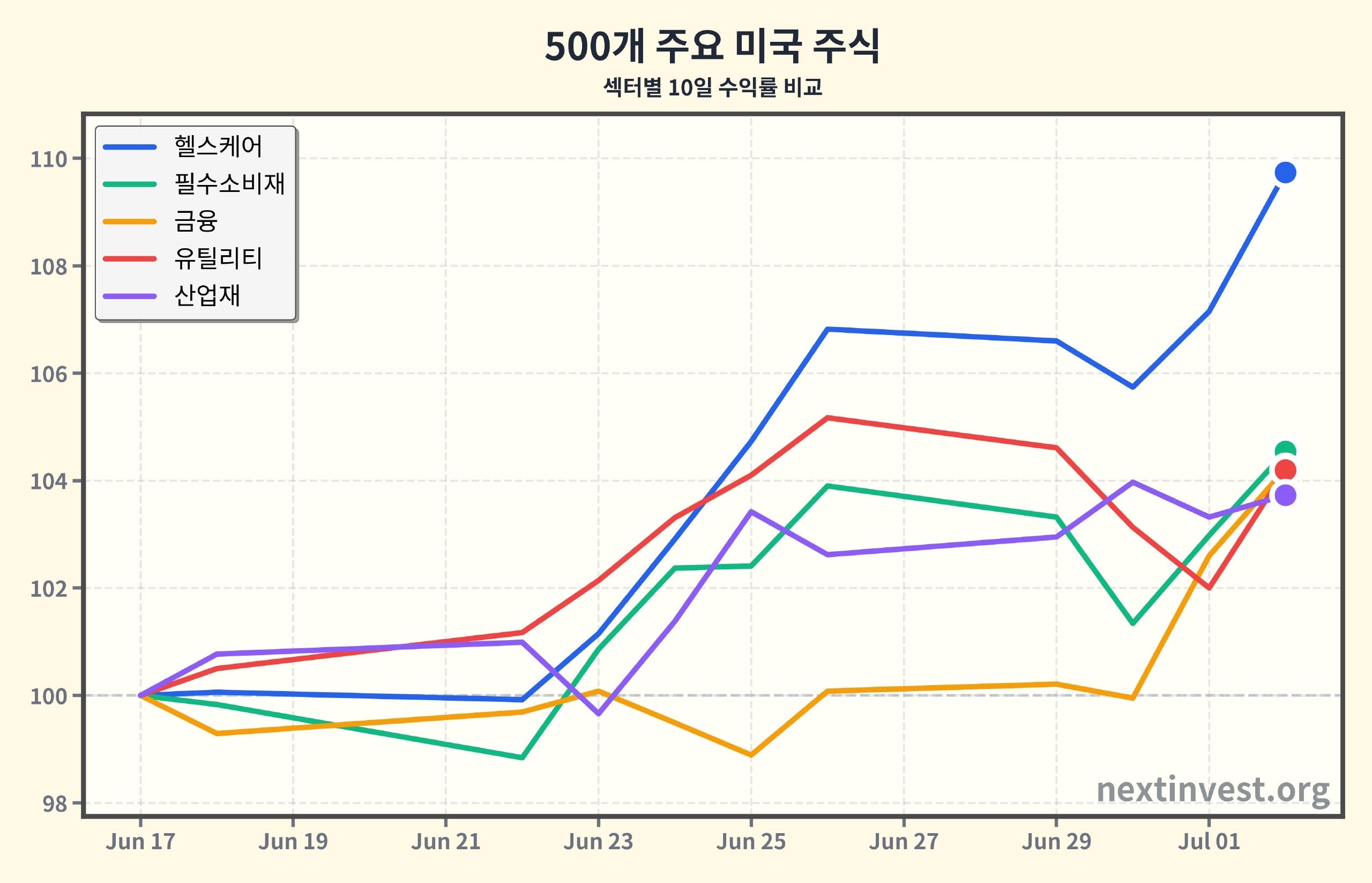

## Sector Performance: Healthcare Leads, Tech Takes a Breather

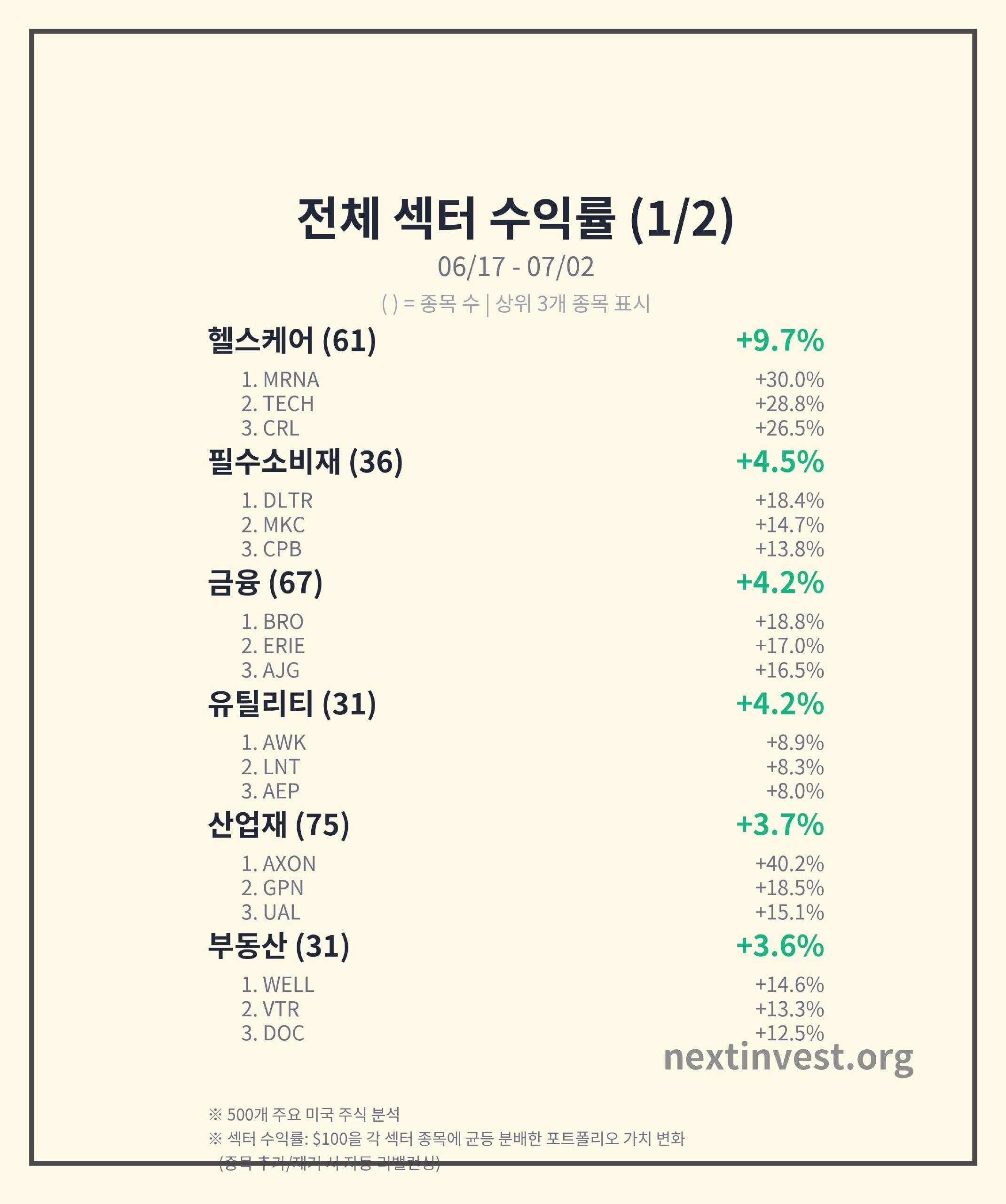

Over 10 trading days (10D), 8 out of 11 sectors were positive, with healthcare leading the pack at +9.74%, while basic materials (-1.74%) and energy (-0.84%) were the weakest.

### 1. Healthcare: Moderna Leads the "Post-Corona" Story

- 10D Return: +9.74% (Sector #1)

- 30D performance was also +12.76%, showing a strong upward trend in both the short and medium term.

- GICS trend analysis shows that the healthcare portfolio has been on an upward trajectory of about +10% since June 22nd.

What happened?

- Leading stock Moderna (MRNA) surged about +30% for the week. Following the FDA advisory committee's positive opinion on Moderna's mRNA flu vaccine in mid-June, and with a final approval decision (PDUFA) approaching on August 5th, the market is re-evaluating the "first visible pipeline" story after COVID-19. (reddit.com)

- The investor community also assesses that "Moderna's rally is no longer a COVID-19 special, but rather a rally based on concrete revenue growth plans and a diverse pipeline of mRNA vaccines and treatments." (reddit.com)

- Other biotech and CRO (contract research organization) companies such as Bio-Techne (TECH) and Charles River Laboratories (CRL) also recorded 20% gains, supporting the sector rally.

Why is it important?

- Healthcare is a defensive sector with consistent demand regardless of the economy. With the addition of new drug and platform momentum, this week showcased both defensive and growth characteristics.

- Looking at the long-term trend, healthcare was up +4.06% over 120D, which was somewhat sluggish. However, this 10D rally could be the beginning of a new trend, breaking away from the previous stagnation.

- For investors, while preparing for economic slowdown and policy uncertainty, healthcare is a sector worth considering if you don't want to give up growth potential. However, individual biotech stocks can be volatile, so ETFs or large-cap stocks may be relatively safer options.

---

### 2. Consumer Defensive: Money Flows into Everyday Necessities

- 10D Return: +4.54%

- 30D: +5.11%, 120D: +7.40% showing a steady upward trend.

- The sector trend analysis shows a gradual upward trend of about +4.6% since June 17th.

Notable Stocks

- Dollar Tree (DLTR): Up over 18%. Discount retailers tend to benefit in a slowing economy as consumers seek value.

- McCormick (MKC), Campbell Soup (CPB): Each up over 10%. As spice and processed food companies, they benefit from increased demand for home cooking and lower-priced food options, and their ability to pass on price increases.

Analysis

- Weakening employment indicators and a prolonged high-interest rate environment are tightening household budgets, leading to increased preference for companies selling low-cost and essential items.

- Considering that both 30D and 120D have consistently shown positive returns, this week's surge appears to be an extension of the defensive stock trend that has been ongoing for several months rather than a one-time event.

---

### 3. Financials, Utilities, Industrials: Rediscovering Stable Cash Flow and Dividends

#### Financial Services

- 10D: +4.22% / 30D: +9.27%, making it the second strongest sector in terms of medium-term momentum.

- Sector trend analysis shows a short-term uptrend (+4% or more) starting on June 30th.

- Insurance and brokerage firms Brown & Brown (BRO), Erie Indemnity (ERIE), and Arthur J. Gallagher (AJG) recorded gains of 15-19%.

- Weakening employment and easing interest rate concerns are reducing the risk of a sharp rise in long-term interest rates while maintaining relatively high interest levels, which is positive for both investment returns and stability for insurance and asset management companies.

#### Utilities

- 10D: +4.20%, 120D: +12.63%, effectively making it a quiet strong performer this year.

- A portfolio-based uptrend of +7.57% has been in place since June 1st.

- Water, electricity, and gas companies (AWK, LNT, AEP) have seen consistent gains.

Why Utilities?

- Utilities are a typical "bond substitute" sector.

- Expectations of interest rate cuts → Bond prices rise + Utility attractiveness increases

- Moreover, demand remains relatively stable even during economic slowdowns, and they have a regulatory framework that ensures stable income.

- With a 120D return of over +12%, utilities are reemerging as a core component of defensive portfolios.

#### Industrials

- 10D: +3.73% / 30D: +10.10% / 120D: +11.20%, indicating consistently strong medium and long-term momentum.

- Sector trend analysis shows an uptrend of +7.44% starting on June 10th.

- Leading stock Axon Enterprise (AXON) surged by approximately +40% over the past 10 days, while some payment and airline stocks (GPN, UAL) also recorded double-digit gains.

In the case of AXON, it is a platform company that encompasses police equipment, body cameras, cloud evidence management, and AI-based software. Following its earnings release in May/June, guidance for 2026 revenue and profits was raised, and expectations for growth in AI-based products have led to a reassessment of the stock's value. (tipranks.com)

While there is still debate within the investment community about its high valuation, this week's movement can be seen as a signal that "confidence in its growth potential is returning." (reddit.com)

---

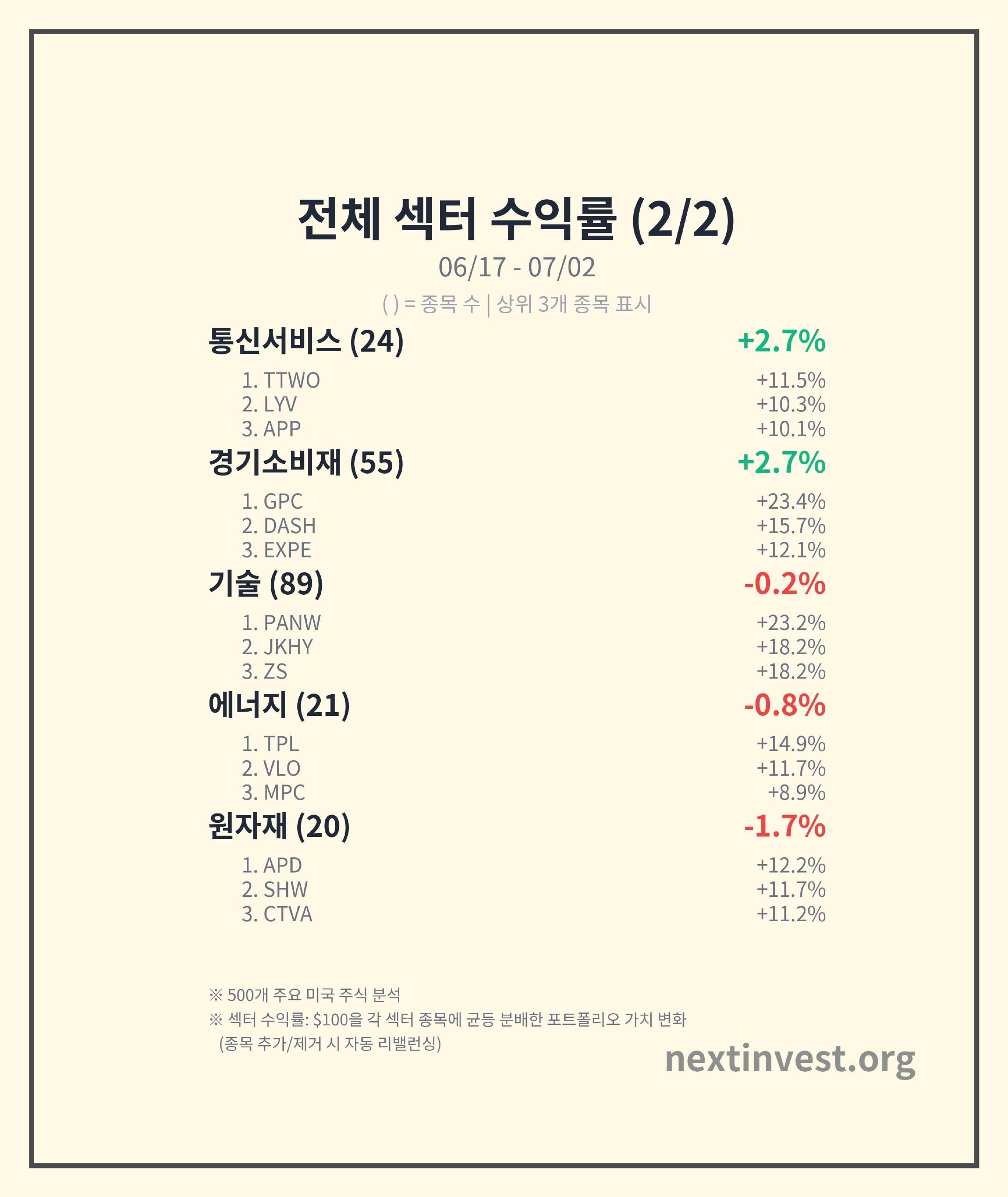

### 4. Communication Services, Consumer Discretionary: Short-Term Rebound, but Long-Term Trends Remain Weak

#### Communication Services

- 10D: +2.71% achieved a short-term rebound, but 30D -2.32%, 120D -7.05% remain negative in the medium and long term.

- Trend analysis shows an approximate -9.5% adjustment between June 1st and 25th, followed by a +5% rebound trend starting on June 25th.

- Gaming, entertainment, and digital advertising stocks (TTWO, LYV, APP) saw gains of around 10%.

Key Points:

- Advertising, entertainment, and games are sensitive areas to economic conditions and consumer sentiment. This week's rebound is linked to improved sentiment due to easing employment indicators → expectations of a soft landing in the economy, but it's important to remember that with 120D still at -7%, this is not yet a trend reversal.

#### Consumer Cyclical

- 10D: +2.70%, 30D: +10.00% - a strong recovery in the past month, but 120D is still at -4.80%, failing to recover the highs seen at the beginning of the year.

- Trend analysis shows a picture of a gentle upward regime (+4.23%) starting on June 3rd, following double-digit declines (-11% etc.) in April and May.

- Strong stocks (GPC, DASH, EXPE) have emerged selectively in cyclical industries such as automobiles, travel, and online services.

Summary

- Both communication and consumer cyclicals share the common characteristic of a short-term rebound versus long-term weakness.

- While interest rate burdens are easing, allowing for a breathing period, these sectors could be hit again if the economic slowdown worsens. Compared to defensive sectors, they carry a higher risk.

---

### 5. Technology, Energy, Basic Materials: Adjusting High Valuations and Cyclical Sectors

#### Technology

- 10D: -0.22% slight decline, and -1.32% in the last session (24H), making it the worst performer.

- However, 120D performance is +29.48%, ranking first among the 11 sectors. This week appears to be a breather after a strong long-term rally.

- Trend analysis also shows that the technology portfolio surged by almost +35% since early April, but has been in a -2.5% adjustment regime since June 12th.

What pressured tech stocks?

- The biggest issue is the adjustment of semiconductor and AI-related stocks. The semiconductor index dropped by about 11% in just two days this week, indicating concentrated profit-taking on AI-related stocks. (ts2.tech)

- Notably, Arm Holdings (ARM) plummeted by over 20% this week. This is due to a combination of high valuation (price-to-sales ratio of 60~70, very high PER), increased R&D costs, and concerns about slowing investment from cloud customers. (ts2.tech)

Nevertheless, some software stocks (PANW, JKHY, ZS) in areas like cybersecurity and fintech showed strong performance of 18~23% over the past 10 days. This highlights a growing temperature difference between individual stocks within the tech sector.

Meaning for Investors

- Rather than signaling an overall decline in technology, it appears to be a price adjustment for some AI and semiconductor names that had become excessively expensive.

- Considering the big picture of 120D +29%, the long-term trend is still upward, but

→ in the short term, selective stock picking within the sector has become more crucial.

#### Energy

- 10D: -0.84%, 30D: -11.42% - the worst performing sector over the past month.

- However, with a 120D performance of +18.84%, the magnitude of the recent decline suggests an adjustment following a period of strong growth.

- Trend analysis also shows that the energy portfolio has been in a downward regime of over -10% since mid-May.

- Some refining and energy infrastructure companies (TPL, VLO, MPC) showed gains of 9~15% over the past 10 days, but this was not enough to reverse the overall sector trend.

#### Basic Materials

- 10D: -1.74% (sector worst performer), 30D is +2.45%, barely positive, but the recent weakness suggests a momentum shift.

- Trend analysis also shows a downward regime of around -2% since June 17th.

- Nevertheless, high-quality chemical and specialty materials companies (APD, SHW, CTVA) recorded double-digit gains, highlighting polarization within the sector.

Summary

- Energy and materials are cyclical stocks sensitive to global demand and commodity prices.

- In the current environment of growing concerns about employment slowdown and downward growth revisions, a defensive rotation rather than overall risk appetite seems to be driving the relative underperformance.

---

## Key Stock Trends: Names That Moved the Market This Week

### 1) Axon Enterprise (AXON) — "When AI Connects to Earnings"

- Up over 40% in the past 10 days, AXON has seen the biggest move in the industrial goods sector.

- The company's business model combines TASER electric shock devices, police body cameras, a cloud-based evidence management platform, and AI-powered analysis and software. This is gaining renewed market appreciation.

- In the May/June earnings release, 2026 revenue and margin guidance was raised, and the growth potential of its AI product line was emphasized. Since early July, there has been a growing perception that "valuation is burdensome, but the growth story remains valid." (tipranks.com)

Meaning:

- This shows that the market is rewarding companies with AI stories that translate into actual products, contracts, and cash flow, rather than just companies that say they "do AI."

### 2) Moderna (MRNA) — First Real Revaluation Since COVID

- Up about 30% in the past 10 days, MRNA led the healthcare sector rally.

- On June 18th, an FDA advisory committee issued a positive opinion on the approval of an mRNA flu vaccine. With the final PDUFA date approaching on August 5th, MRNA is undergoing a revaluation from a one-time COVID beneficiary to a diversified vaccine and therapeutics platform company. (reddit.com)

Meaning:

- Pharmaceutical and biotech investments often feel like betting on a "dream," but...

→ As regulatory timelines, clinical data, and concrete revenue guidance accumulate, the growth story is translated into numbers, leading to a redefinition of valuation.

### 3) Arm Holdings (ARM) — Valuation's Counterattack

- Down about 25% in the past 10 days, ARM was a symbolic name for the tech sector weakness.

- With a PER still around 60~70 times revenue, reflecting extreme AI expectations...

→ Increased R&D costs, delays in investments from cloud customers, and uncertainties regarding production capacity have fueled selling pressure. (ts2.tech)

Meaning:

- "Good companies" and "good investments" are not always the same.

- This adjustment serves as a warning that valuation and risk management are even more crucial for stocks at the heart of the AI boom.

---

## Key Points to Watch Next Week: Defensive Stocks Rally vs. Growth Stocks Comeback

### 1. Macro and Policy

- This week's employment data led the market to believe that "the possibility of an additional rate hike in July is low." (ethivo-briefing.com)

- Next week, the market's attention will be focused on inflation indicators such as CPI and PCE.

→ If inflation cools faster than expected...

- The current preference for defensive stocks and dividend payers could strengthen further,

- Some growth stocks (especially high-yield software, healthcare, and quality tech) could be revalued as a combination of "growth + stability."

### 2. Sector Checkpoints

- Healthcare, consumer staples, utilities, financials:

- Already up significantly over the past 30 days, so be mindful of potential short-term speed adjustments.

- However, as long as concerns about employment and growth slowdown persist, they are likely to maintain their mid-term defensive role.

- Technology, semiconductors:

- Whether the adjustment in high-valuation stocks like ARM will lead to a sector-wide sell-off or an internal rotation towards better tech stocks with less valuation burden is key.

- Tech portfolios are already up 29% over the past 120 days, so a more rational approach would be to adjust and diversify rather than chase further gains.

- Energy & Materials:

- If the recent month-long slump extends, it could signal growing concerns about economic slowdown.

- Conversely, if oil and raw material prices rebound, there is also a possibility that bargain-buying capital could flow into energy and materials.

### 3. Summary for Individual Investors

1. Checking Your Portfolio's Defensive Strength

- This week's flow is a typical defensive rotation of "selling tech to buy healthcare, consumer staples, and utilities."

- If your portfolio is heavily concentrated in growth stocks, it may be time to diversify some allocation to sectors with stable cash flow.

2. AI & High-Growth Stocks: Time for Stock-by-Stock Selection

- The stock price movements of companies like Axon, which are backed by actual earnings and products, and companies like ARM, which face significant valuation debates, are diverging significantly.

- This can be read as a message not to lump them together just by the name "AI theme," but to separately examine each company's numbers and valuation.

3. Look at the Long Trend, Not Short-Term News

- Healthcare might appear to have suddenly jumped out when looking only at this week, but when viewing the 30D and 120D along with the provided sector regime, you can see it's a movement riding on the trend built up during April to June.

- Going forward, it would be good to develop a habit of comparing 10D (short-term) vs. 30D and 120D (medium to long-term) each week to distinguish between "noise" and "real trends."

---

In short, this week's market was characterized by "profit-taking and defensive rotation happening simultaneously amid easing interest rate concerns."

Whether this rotation continues next week alongside employment and inflation data, or whether focus returns to growth stocks, will be a key variable in early third-quarter investment strategy.

This content is provided for informational purposes only and does not constitute an investment recommendation for any specific stocks or assets.

Source: https://nextinvest.org/ko

You can share freely without permission ^^