Where are we now

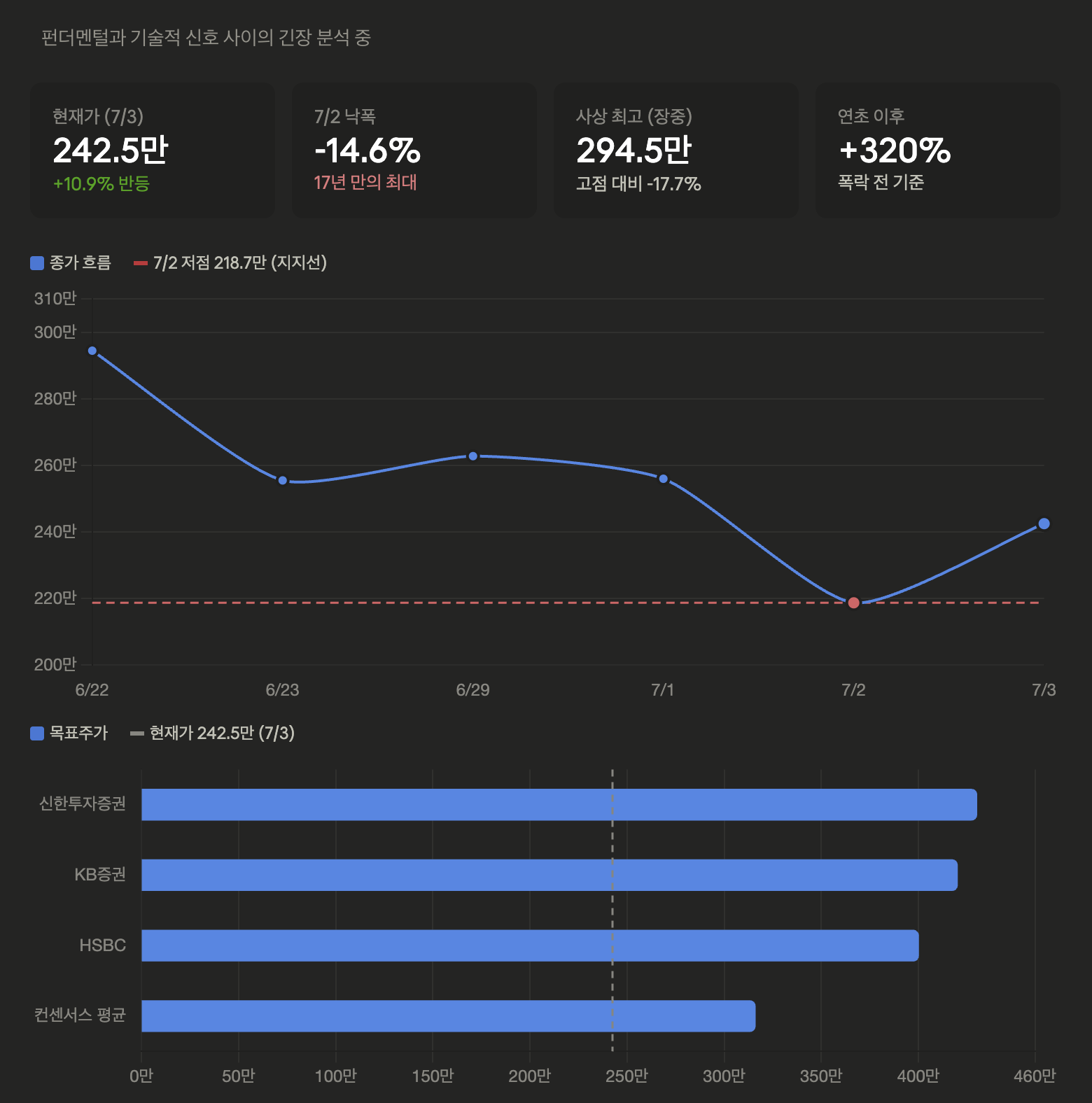

First, the facts. SK Hynix closed at 2,187,000 won on July 2nd, a 14.57% plunge, marking its biggest drop in 17 years since the 2008 financial crisis. And today, July 3rd, it's trading around 2,425,000 won, rebounding about 11%. A one-day -14.6% → +11%, that's the kind of volatility you see in KOSDAQ theme stocks, not large caps. EtodayInvesting.com

The trigger for the plunge wasn't fundamentals but narrative. Meta announced its plan to lease excess computing resources secured during AI infrastructure development to external customers, sparking concerns about Big Tech overinvestment and potential peak demand for semiconductors. This sentiment then spilled over from Micron's decline → domestic semiconductor investment selling. In the background, SK Hynix had already surged nearly 16 times from around 170,000 won early last year, exceeding 320% this year alone, reaching the top market cap and hitting an all-time high (intraday trading in the 294,000 won range) – milestones achieved simultaneously. There was also a concentration of profit-taking orders as it had already risen significantly. Looking at supply and demand, foreign investors net sold SK Hynix by 2.4 trillion won over two days in July, while individual investors net bought 4.5627 trillion won.

Herald Corp + 2The Calendar Ahead — July is the Deciding Month

July is packed with events.

7/10 Nasdaq ADR listing (target date). Issuing 17.79 million new shares to raise approximately $29 billion (45 trillion won) raises dilution concerns, but it's also a key argument for the bullish thesis. HSBC raised its PBR from 2.8x to 3.4x and its target price from 2,900,000 won to 4,000,000 won (a 38% increase) based on the expectation that the Nasdaq listing will change valuation standards. They also cited Micron's average 35% higher valuation compared to Hynix over the past 13 years due to US investor accessibility as a catalyst for narrowing the gap. However, it's important to note that indices like the Philadelphia Semiconductor Index are based on stocks listed for three months or more, making inclusion in the regular September update unlikely.

Newsfc + 37/29 Q2 earnings. Shinhan Investment Securities forecasts Q2 revenue of 8,826.3 billion won and operating profit of 6,676.3 billion won, while KB Securities projects Q2 operating profit to increase eightfold year-on-year to 69 trillion won, followed by 83 trillion won in Q3 and 91 trillion won in Q4. The numbers themselves are still monstrous.

EtodayDaumLong-term supply and demand logic. While DRAM and NAND wafer production capacity growth rates are projected to be 7% and 4%, respectively, by 2027, demand growth rates are expected to be 17% and 19%, respectively, further exacerbating the supply shortage. This is the backbone of the bullish thesis. KB Securities raised its target price to 4,200,000 won based on the outlook for prolonged memory supply shortages until 2028. The consensus also reflects overwhelming optimism, with an average 12-month target price of 3,159,913 won and 35 analysts recommending buy versus one sell recommendation.

Etoday + 2Risks include the potential for a resurgence of the Meta overinvestment narrative, reports of MSCI inclusion failure, and macro factors such as a possible US interest rate hike in the second half leading to a rise in the won/dollar exchange rate to around 1,530 won. There's also dilution from ADR new shares.

EBC Financial GroupThrough the Mark Minervini Lens — This is Key

Let's be honest, scenario investors. Brokerage firms' target prices of 4,200,000 won and 4,300,000 won are based on fundamentals. But Minervini would first look at price action. And this week's chart sends a clear warning signal.

Parabolically up 320% stock accompanied by heavy trading recorded a daily -14.6%, the largest drop in 17 years — this is a typical > and breakdown signal after a climactic run, according to Minervini terminology. As he always emphasizes: the reason (meta news) is not important, the fact that the stock price reacted that way is information itself. Today's +11% rebound also cannot rule out the possibility of a reflex rally the day after the crash. The real confirmation points are whether (1) the rebound will come with less trading volume than the decline, (2) whether it will maintain the low point (2.18 million shares) and build a base again, and (3) whether it will recover the high point even after digesting the events of 7/10 ADR and 7/29 earnings announcement.

To put it in SEPA terms, this is not a "confident entry zone" but rather a "zone for watching with hands in pockets and observing the formation of a new base." If you have an ongoing position, maintain exposure only as much as the market proves, according to the progressive exposure principle. Of course, there is also a strong view that "only the narrative has been damaged, profits are solid, and the crash reflects a leading PER of around 7x, making it a buying opportunity," like Kiwoom Securities — this is the exact picture where fundamental strength and technical caution collide.

Finally, Kong's obligatory comment: I am not an investment advisor, and the above content is for informational purposes only and not investment advice. If you include 2.2 million support in your scenario and set 7/10 and 7/29 as two breakpoints, your judgment will be much clearer. Seeing that an individual received 4.5 trillion won yesterday, it seems that the beast's heart is not only yours.