6/25 U.S. Stock Market — Industrials & Healthcare Lead, Large-Cap Tech Takes a Breather

June 25, 2026 Market Analysis

## 1. Today's Market at a Glance

June 25 was another day that illustrated the "rotation of money" in U.S. equity markets. With strong semiconductor earnings and still-elevated inflation signals colliding, the major indexes delivered mixed results, but sector-level flows clearly shifted toward industrials, healthcare, and energy.

- Index summary: The Dow rose approximately +1%, the S&P 500 edged slightly higher, and the Nasdaq closed down roughly -0.5%.(marketscreener.com)

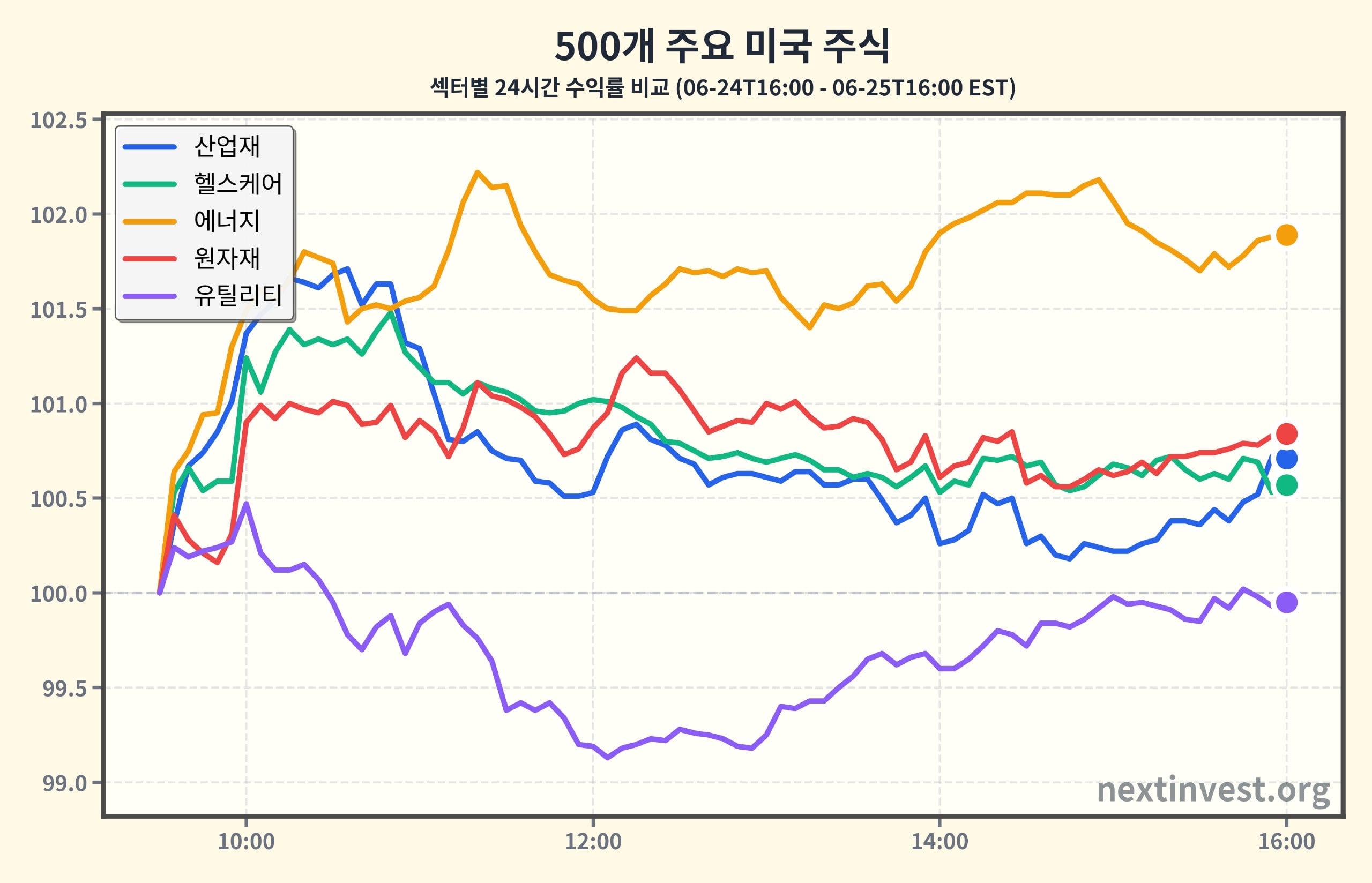

- Today's sector performance (based on your portfolio):

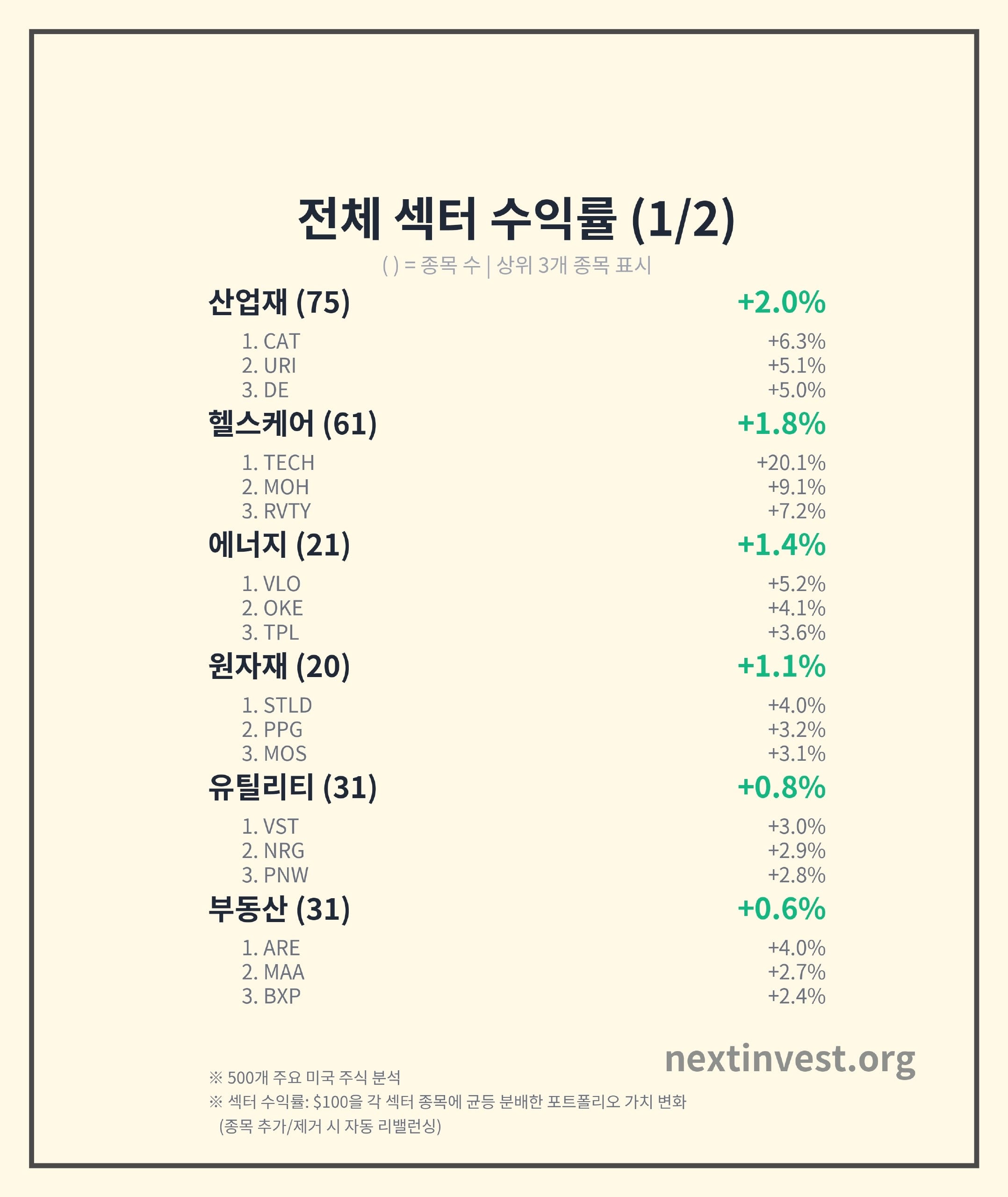

- Top gainers: Industrials (+1.98%), Healthcare (+1.79%), Energy (+1.39%), Basic Materials (+1.11%), Utilities (+0.84%), REITs (+0.58%), Consumer Staples (+0.02%)

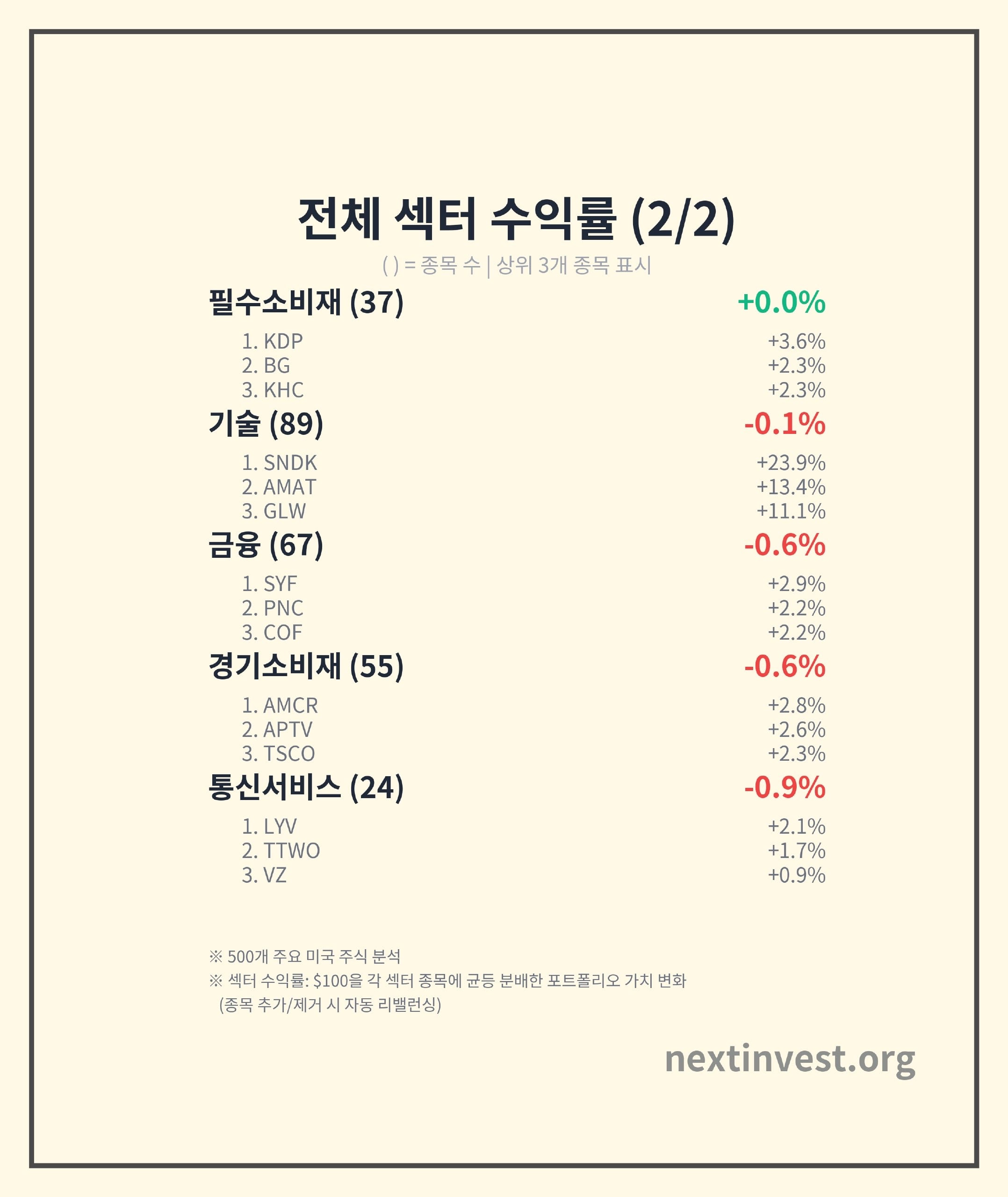

- Decliners: IT (-0.08%), Financials (-0.62%), Consumer Discretionary (-0.63%), Communication Services (-0.91%)

Key message:

The mega-cap tech and AI themes that have driven the market higher in recent months are pausing to catch their breath, while capital is visibly rotating into industrials, energy, and healthcare — sectors more closely tied to the real economy.

---

## 2. Tech Stocks: Semiconductors Surge, Big Tech Consolidates

### 2-1. What Happened Today

- Sector return (24H): Technology -0.08% (volatility 4.44%)

- Notable gainers:

- Sandisk (SNDK): +23.92%

- Applied Materials (AMAT): +13.42%

- Corning (GLW): +11.09%

Background news

- Micron's explosive earnings and guidance, reported the prior day, provided strong upward momentum through the early part of today's session.

- Analysis showed Q3 revenue of approximately $41.4 billion, adjusted EPS of roughly $25, and revenue more than tripling year-over-year, with next-quarter revenue guidance of around $50 billion — confirming that AI memory demand remains explosive.(m.ajupress.com)

- In the wake of these results, not only Micron but also SNDK, Western Digital, and other memory and storage-related stocks surged sharply even before the open.(m.ajupress.com)

- On a global level, the strong semiconductor earnings were also assessed as a catalyst lifting equity markets worldwide.(marketscreener.com)

Despite all this, the sector as a whole finished down -0.08%. Memory and equipment stocks rallied, but profit-taking in the mega-cap platform, cloud, and software names that had run up the most weighed on the overall index. Reuters and other outlets interpret this as a "rebalancing driven by valuation pressure."(investing.com)

### 2-2. Viewing This Within the Short- and Medium-Term Trend

- 7-day trend:

- 6/18 +1.50% → 6/22 +0.27% → 6/23 -2.96% → 6/24 +0.43% → 6/25 -0.08%

→ After a brief recovery early in the week, a sharp pullback on the 23rd was followed by a mild plus, near-flat, then slightly negative close — a pattern suggesting fading momentum.

- Medium-term trend (portfolio analysis):

- From a base of 100 on 3/31, the sector now stands at 134.39 — up approximately +34%, still the dominant outperformer over this period.

- After a strong rally from mid-May (5/19–6/4: +14.9%), the sector has gained only about +1.6% since June 5, indicating a significant deceleration in pace.

### 2-3. What This Means for Investors

- If you already carry a large allocation to AI, semiconductors, and big tech:

- A session like today — where earnings are strong yet stocks fail to lift the broader market — can be a signal that the market says "we believe the growth story, but the price is too high."

- Keep in mind the potential for increased short-term volatility and range-bound trading, and scrutinize individual company earnings and valuations more carefully.

- If your IT exposure is still low:

- This consolidation could represent a "dollar-cost averaging opportunity during the breather" for long-term investors. That said, rather than a broad sector ETF, it is more advantageous for risk management to focus selectively on semiconductor, equipment, and specific infrastructure companies where cash flow and earnings are actually growing rapidly.

---

## 3. Industrials & Healthcare: Today's Real Stars

### 3-1. Industrials: Money Moves into Cyclicals

- Today's performance: +1.98% (volatility 2.50%). Of the past 7 trading days, the sector gained on four — 6/18, 6/22, 6/24, and 6/25 — making the upward trend this week quite clear.

- Notable stocks:

- Caterpillar (CAT): +6.29%

- United Rentals (URI): +5.15%

- Deere (DE): +5.00%

All of these companies are directly linked to real-economy investment and global cyclical recovery — construction, heavy equipment, infrastructure, and agricultural machinery. Multiple market commentaries explain that some capital is rotating out of recently corrected tech stocks into cyclical names with stable medium-to-long-term growth stories.(finlore.io)

- Medium-term trend:

- The industrials sector portfolio is up +11.9% since 3/31.

- After a steady, gradual uptrend since 5/18, the sector has added nearly +3% over just the past two days (6/24–25), with recent momentum clearly strengthening.

What does this suggest?

> It is a signal that the market is saying "AI alone is not enough to build a portfolio" and is diversifying risk into sectors tied to the real economy and infrastructure.

- From a long-term investment perspective, gradually increasing exposure to industrials/infrastructure-related ETFs or high-quality individual stocks can help reduce overall portfolio volatility.

### 3-2. Healthcare: Spotlight on a Major M&A Deal

- Today's performance: +1.79% (volatility 2.58%)

- Notable surge:

- Bio‑Techne (TECH): +20.07%

The catalyst was a major acquisition announcement.

- Germany's Merck KGaA agreed to acquire U.S. biotech and diagnostics company Bio‑Techne for approximately $11.3 billion.(fiercepharma.com)

- The offer price represents a premium of approximately 36% over the average share price of the past month, illustrating how strategically the market values this company.(fiercepharma.com)

- Bio‑Techne has served as an "essential component supplier" to the research and biopharmaceutical industry — providing cell therapy products, antibodies, and diagnostic reagents.(cbsnews.com)

The healthcare sector gained only +9% over the past 60 trading days, but has risen +4.9% in just the current window since 6/22, with short-term momentum rapidly reviving.

What this means for investors

- It suggests that the environment where investors are willing to pay high valuations for companies with proven growth stories — as seen in big tech and semiconductors — is now expanding into healthcare and life sciences.

- Healthcare, which has a relatively low correlation with the economic cycle,

- can offer both portfolio defense (defensive) and growth optionality simultaneously,

- and a large M&A deal like today's can raise the prospect of revaluation for similar mid-cap biotech and diagnostics companies ("could they be the next acquisition target?").

---

## 4. Energy, Basic Materials & Utilities: A Window Into Inflation and Rate Expectations

### 4-1. Energy: A Single-Day Bounce Within a Downtrend

- Today's performance: +1.39%

- VLO +5.21%, OKE +4.14%, TPL +3.57% — refiners, pipelines, and energy royalty names led the gains.

- However, the cumulative return since 3/31 stands at -8.75%, the worst among all 11 sectors.

- Looking only at the period since 5/18, the sector is down -8.8% in an ongoing downtrend — today's bounce is just that, a single-day rebound within that trend.

International oil prices and commodity prices have been weak amid a mix of growth slowdown concerns and supply factors, and some reports interpret this as "a signal that inflationary pressure is gradually easing."(finlore.io)

Implications:

- Energy stocks can be attractive for dividends and cash flow, but the sector swings sharply on oil prices, policy, and geopolitical risk.

- Today's action looks more like short covering and a technical bounce — it is too early to call an end to the medium-term downtrend.

### 4-2. Basic Materials & Utilities: Capturing Real Demand and Rate Sensitivity Simultaneously

- Basic Materials: +1.11% today; names like STLD, PPG, and MOS — steel, coatings, and fertilizers — are structurally tied to industrial demand and agricultural/infrastructure investment.

- Over the past 60 days, however, the gain is a modest +1.6%, and the sector has been in a -1.2% downtrend since 5/27.

- Utilities: +0.84% today; the sector has quietly gained +7.5% since 6/1, maintaining a steady under-the-radar bull run.

From an interest rate perspective:

- The 10-year U.S. Treasury yield edged slightly lower today to around 4.38%, as the market simultaneously prices in the possibility of slowing growth and an extended period of elevated rates.(finlore.io)

- The fact that rate-sensitive utilities and REITs (real estate) have been quietly strengthening over the past few weeks can be read as:

- the market expectation that "growth will be maintained, but aggressively hiking rates further as in the past is too much of a burden" is gradually being priced in.

---

## 5. Financials, Consumer & Communication Services: Sectors Quietly Falling Behind

### 5-1. Financials: A Tug-of-War Between Rates and the Economy

- Today's performance: -0.62%

- Even so, select individual names such as SYF, PNC, and COF — some bank and card stocks — posted gains of around 2%.

- The 60-day cumulative return of +8.7% is respectable, but since 6/16 the sector has shifted into a -1.9% declining trend.

Market participants report that because key inflation indicators such as core PCE are still coming in elevated,

- the view that "it is difficult to expect large rate cuts anytime soon" and

- the view that "further tightening to cool the economy further is too burdensome" are coexisting.(reddit.com)

In this ambiguous environment, the financial sector is becoming a "neutral" sector that finds it difficult to move strongly in either direction.

### 5-2. Consumer Sectors: Staples Steady, Discretionary on a Rollercoaster

- Consumer Staples: essentially flat at +0.02% today.

- Food and beverage names such as KDP, BG, and KHC posted gains of 2–3%, once again demonstrating the stability of consumption that is independent of the economic cycle.

- Consumer Discretionary: -0.63% today, essentially a pullback from the sharp +2.21% surge the prior day (6/24).

Looking at the 7-day trend, Consumer Discretionary moved +1.33% → -1.29% → -0.24% → +2.21% → -0.63% — up one day, down the next, behaving like a "sector with extreme mood swings."

> A polarized consumer environment — where financially robust households and financially stressed households coexist simultaneously — is being reflected directly in stock prices.

### 5-3. Communication Services: Correction in Advertising, Entertainment & Platforms

- Today's performance: -0.91% (volatility 2.51%)

- The 60-day return is also -3.5%, and the sector is down -9.5% in just the period since 6/1 — a clear downtrend.

This sector is a mix of large platforms, telecoms, media, entertainment, and gaming, facing a combination of:

- valuation pressure across tech and growth stocks broadly,

- concerns about a slowdown in the advertising cycle, and

- intensifying competition in subscriptions and content.

For investors, the need to distinguish between companies where the growth story remains valid and those where near-term earnings are decelerating has grown substantially in this phase.

---

## 6. Summing Up Today From a Portfolio Perspective

### 6-1. The Big Picture: Not 'Abandoning AI,' But 'Not Relying on AI Alone'

Synthesizing today's news and numbers, the market can be interpreted as acknowledging the long-term growth potential of AI and semiconductors while correcting the portions of the market that have risen too far, too fast.(investing.com)

- Short-term (7-day) basis:

- Industrials, healthcare, utilities, and REITs are quietly trending upward,

- while IT, communication services, and financials show weak directionality or are tilting lower.

- Medium-term (60-day) basis:

- IT remains the sector with the largest cumulative gain (+34%), but the pace of the rally has slowed.

- Industrials, healthcare, and utilities are showing a gradual but steady upward trend, serving as the "pillars" of the portfolio.

### 6-2. Practical Implications for Investors

1. The case for sector diversification strengthens

- On days like today — when "earnings are good but the indexes are mixed" — sector composition, more than individual themes or stocks, determines returns.

- If you already carry a heavy weight in IT and communication services, now may be the right time to consider diversifying a portion into industrials, healthcare, utilities, and consumer staples.

2. M&A and earnings create 'hidden winners'

- Mid-cap companies that play a critical infrastructure or platform role — like Bio‑Techne — are natural acquisition targets for large corporations.

- Rather than simply saying "it's biotech, so it's risky," the perspective of asking whether a company provides essential equipment, materials, or services to an industry is becoming increasingly important.

3. Rates and inflation: 'High, but too burdensome to raise further'

- Even as inflation indicators are cited as still elevated, the market is pricing in the prospect of rates staying higher for longer.(reddit.com)

- In this environment, utilities, REITs, select energy names, and consumer staples — with stable dividends and cash flows — serve as a buffer to balance out aggressive growth stocks.

---

## 7. Closing: Points to Watch as We Prepare for Tomorrow

1. The 'second-order beneficiaries' of the AI and semiconductor rally

- The strong results and surges in Micron, SNDK, AMAT, and others ripple through the entire upstream and downstream ecosystem for storing, transmitting, and processing data — materials, equipment, and infrastructure.

- Rather than chasing short-term spikes, a better approach is to ask: "If this demand persists for 3–5 years, which companies will earn money most reliably?"

2. Confirming the 'sustainability' of industrials, healthcare, and utilities

- Whether the three sectors that led today's gains maintain their relative strength this week and next

- could be a clue for judging whether the market has truly begun a structural rotation from "big tech → real economy and defensives."

3. Upcoming inflation and employment data

- Forthcoming indicators such as PCE inflation — the Fed's most closely watched measure —

- will help gauge which way the weight tilts: "prolonged high rates vs. a gradual easing."

- This will have a direct impact on bank valuations, REITs, and growth stock valuations alike.

Today was a day when industrials, healthcare, energy, and utilities quietly elevated their standing while mega-cap tech paused to catch its breath.

For long-term investors, it is a day worth remembering as one that confirmed the signal: "This is no longer a market that belongs to AI alone."

This content has been prepared for informational purposes only and does not constitute a recommendation to invest in any specific stock or asset.

Source: https://nextinvest.org/ko

Feel free to share without permission ^^