3/22 US Stock Market Weekly Analysis - Oil Prices Soaring, Growth Stocks Hit the Brakes

March 22, 2026 Weekly Market Analysis

## This Week's Key Theme: "Oil Rises, Interest Rate Worries Revive"

This week (as of the close on March 22), the US stock market was generally weak. Of the 11 sectors, only energy was positive, while all the rest were negative. The reason is simple.

1. Oil Surge → Renewed Inflation/Interest Rate Concerns

WTI (West Texas Intermediate) crude prices rose to around $98 per barrel, surging roughly 47% this month alone.(kiplinger.com)

- When oil prices rise, the cost of logistics, heating, jet fuel, and overall living expenses goes up, raising fears that inflation could heat up again.

- If inflation reheats, it becomes difficult for the Federal Reserve (Fed) to cut rates, and the possibility of additional hikes even starts to be discussed. In fact, the US 10-year Treasury yield jumped to the 4.3% range.(kiplinger.com)

2. Anxiety That "Money Could Get More Expensive" → Damage to Growth and Consumer Stocks

Signals that interest rates may stay high or rise further weigh on technology and high-valuation growth stocks that depend on future growth, as well as consumer-related sectors.

- Put simply, the value of "future earnings" gets discounted, so the expensive price tags attached to growth stocks come under scrutiny again.

3. Volatility Amplified by Individual Negative News

- Super Micro Computer (SMCI), a flagship AI server stock, plunged more than 30% in a single day as allegations of violating China export controls combined with concerns over investigations and regulations.(kiplinger.com)

- Paramount Skydance (PSKY) saw investor sentiment freeze as its plan to acquire Warner Bros. Discovery led to a massive debt burden and credit rating downgrade (junk grade) issues.(reddit.com)

So why does it matter?

- Oil prices and interest rates are directly tied to real living costs, loan interest, and corporate investment expenses.

- Energy had already surged +31% on a 120-day (about 6-month) basis, and this week its image as an "inflation-beneficiary sector" was further reinforced.

- Conversely, sectors sensitive to the economy and consumption are again pricing in "a world where interest burdens grow heavier."

---

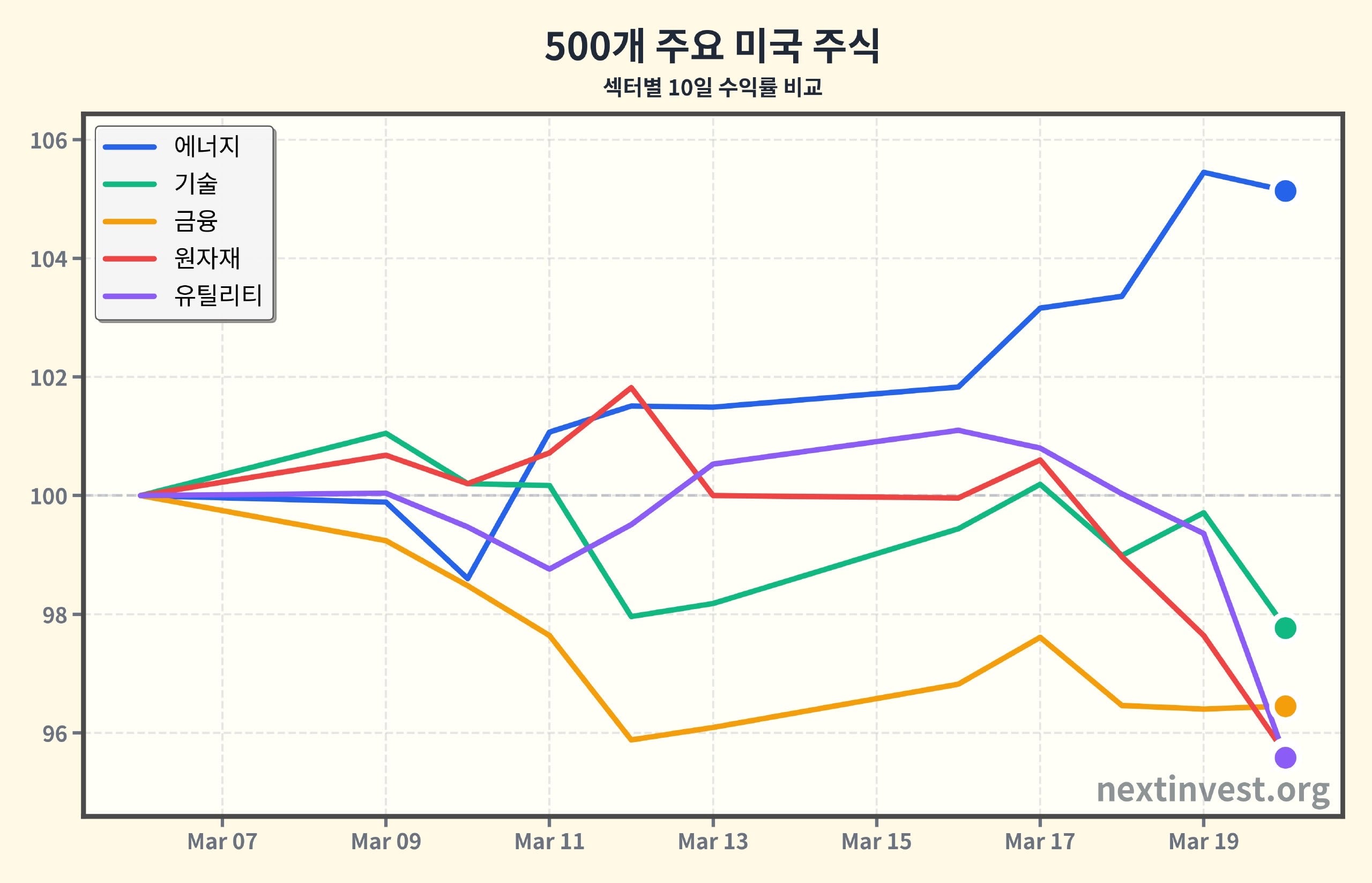

## Sector Performance: A Week Where Only Energy Smiled, While Even Defensive Stocks Shook

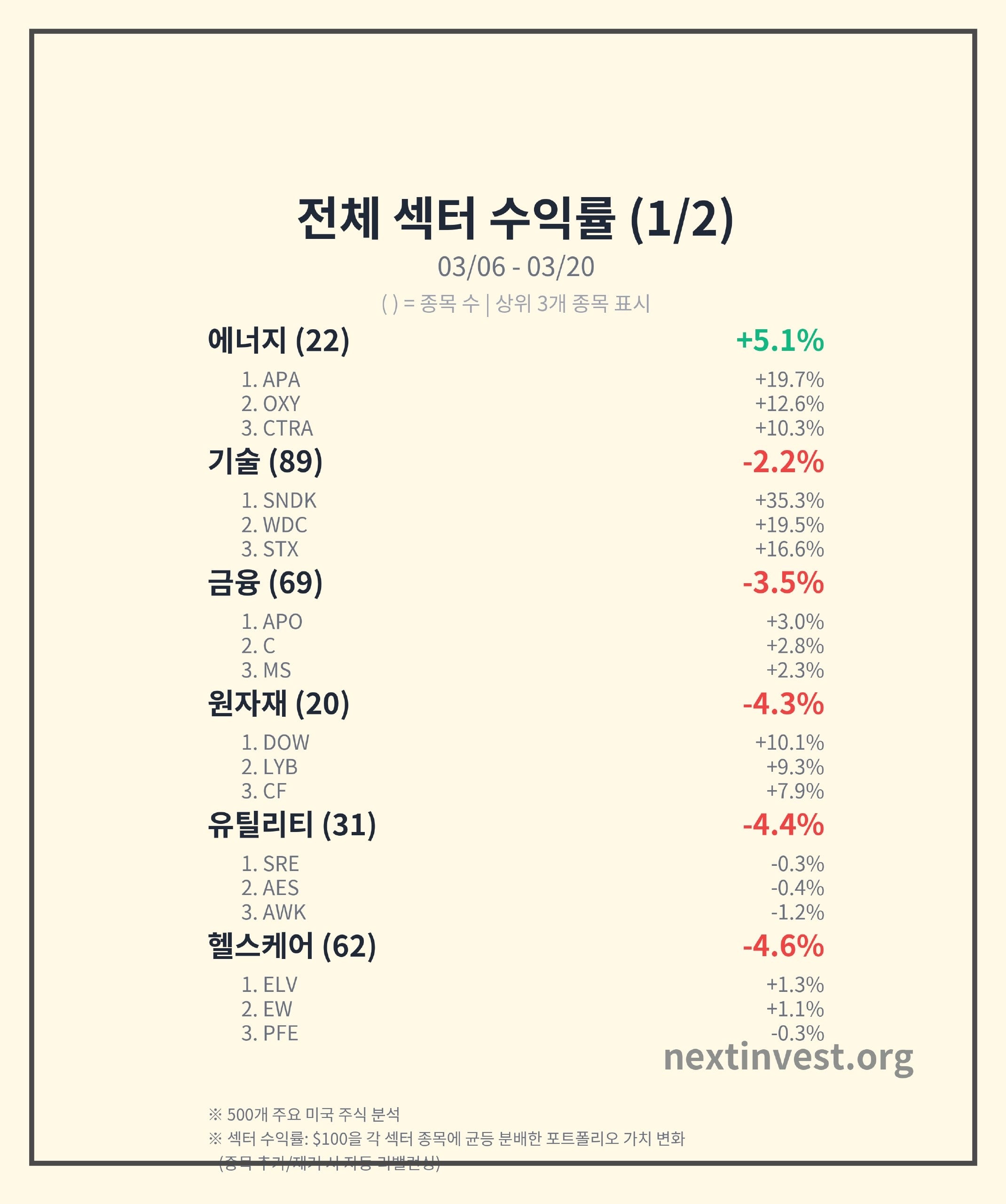

### 1. Energy: Biggest Beneficiary of the Oil Rally (10D +5.14%, 30D +16.89%, 120D +31.17%)

- What happened?

The oil price surge that continued throughout this month carried on this week as well, lifting energy company stocks together.(kiplinger.com)

- With oil-producing nations adjusting supply and geopolitical risks in the Middle East, the perception that "oil could become scarce" has strengthened.

- Key stock movements

- APA (APA): +19.68%

- Occidental (OXY): +12.57%

- Coterra (CTRA): +10.26% — a US E&P company that holds both natural gas and crude oil assets, making it a direct beneficiary of rising commodity prices.(en.wikipedia.org)

- Trend perspective

- Looking at the 30D and 120D performance, energy's strength is not a new rebound but an extension of an uptrend that has continued for several months.

- In other words, this week was closer to a period where the energy sector "reconfirmed its trend."

- Why does it matter to me?

- Continually rising oil prices mean gas stations, airfare, and heating bills could get more expensive.

- In the stock market, "energy is treated like insurance for the age of inflation," and it's a time to consider how much weight to give it in a portfolio.

---

### 2. Technology: Index at -2.23%, Extreme Divergence by Stock

- The sector as a whole was weak at -2.23% on a 10-day basis, but breaking it down internally revealed severe polarization.

- Surging stocks: Storage and infrastructure names

- Sandisk (SNDK): +35.33%

- Western Digital (WDC): +19.51%

- Seagate (STX): +16.56%

→ Amid expectations of expanding demand for AI servers and data centers, the outlook that demand for storage devices (SSD/HDD) will structurally increase was highlighted again.

- Plunging stock: Super Micro Computer (SMCI) -34.85%

- SMCI, formerly a flagship AI server stock, suffered a major shock—falling more than 30% in a single day—as allegations of legal violations related to server exports to China, regulatory risks, and concerns over profitability and accounting transparency all converged.(kiplinger.com)

- For investors, this is a signal that we have moved from the simple story that "the AI boom lifts all related stocks" to a stage of reassessing risks on a company-by-company basis.

- Trend perspective

- The 120D performance is +5.27%, so the mid-term trend is still positive.

- However, the recent 30D is nearly flat (-0.23%) → it looks more like a picture where, with the uptrend pausing for breath, individual bad news this week struck and widened the correction.

- Why does it matter to me?

- AI and digital infrastructure remain important long-term growth themes, but this reminds us of the risk that "stocks bought too expensively" or "stocks with regulatory/accounting issues" can shake significantly.

- It's a lesson that, rather than chasing buys based on the growth story alone, one must also check financial health and regulatory risks.

---

### 3. Financials: Held Up Despite the Renewed Rate Rise (10D -3.55%, 24H +0.08%)

- The sector as a whole was weak at -3.55% on a 10D basis, but the final day (24H) was slightly positive.

- Among the key stocks,

- Apollo Global Management (APO): +3.04%

- Citigroup (C): +2.81%

- Morgan Stanley (MS): +2.33%

some financial stocks were actually firm.

- Why?

- When interest rates stay high, interest income from loans increases, which can also benefit banks and asset managers.

- However, a surge in long-term rates increases the possibility of an economic slowdown and defaults, making it a two-sided environment for the sector overall—"profits may rise, but risks also grow."

- Trend perspective

- Both 30D and 120D are in the -7% range, so it remains in a downtrend over the mid-term.

- This week's weakness is closer to an extension of the existing downtrend, and the slight rebound on a 24H basis is still hard to view as a "trend reversal."

---

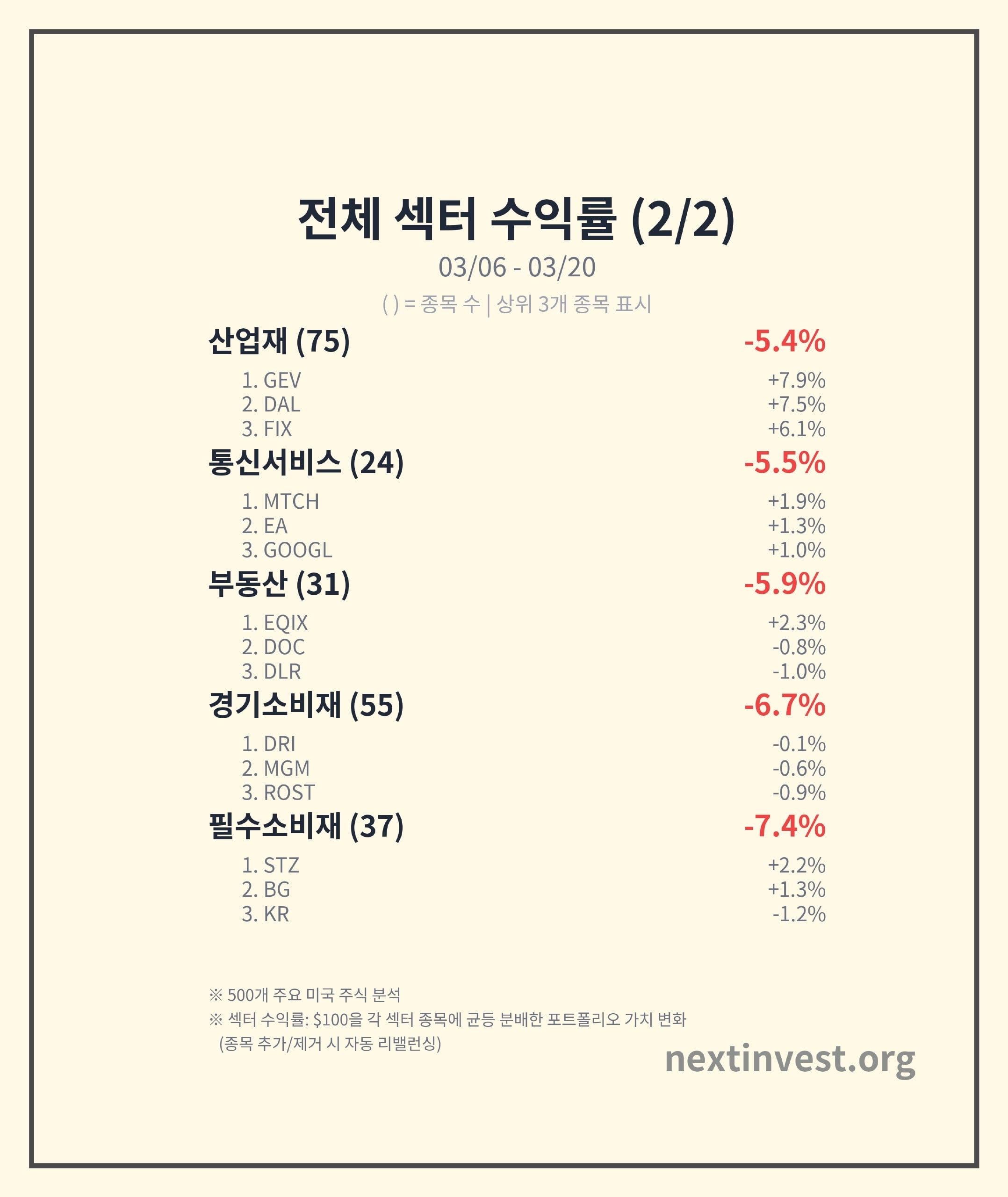

### 4. Consumer/Communication/REITs: Direct Hit from Interest Rate and Debt Burdens

#### Consumer-related (Consumer Cyclical -6.73%, Consumer Defensive -7.39%)

- The economy-sensitive consumer sector (Consumer Cyclical) fell sharply at -6.73%.

- Darden Restaurants (DRI), MGM Resorts (MGM), and Ross Stores (ROST) all held on with slight declines, but the sector as a whole reflected "recession fears + interest burdens" simultaneously.

- Defensive stocks (Consumer Defensive) actually performed worse, at -7.39%.

- Generally, during economic uncertainty, food and consumer staples companies play a defensive role, but this time their shield role weakened as debt burdens and the reassessment of high valuations overlapped.

- Why does it matter to me?

- When interest rates stay high, households face increased loan interest and essential spending, creating an environment where it's easy to cut back on discretionary consumption like dining out, travel, and shopping.

- From an individual investor's standpoint, it's worth remembering that even "defensive stocks" can shake just as much depending on the interest rate and debt structure.

#### Communication Services (-5.46%)

- The sector was weak at -5.46%.

- Among them, Paramount Skydance (PSKY) fell sharply by about -23%:

- Concerns that combined net debt could soar to around $70–80 billion due to the acquisition of Warner Bros. Discovery,(reddit.com)

- Fitch's downgrade to junk (speculative) grade and the possibility of further downgrades,(reddit.com)

- As restructuring of the CBS/streaming business and cost-cutting issues overlapped, investors began to see it as a "media dinosaur crushed by debt."(reddit.com)

- So what changes?

- The media/streaming industry is already fiercely competitive, and the structure means taking on a bigger body along with heavier debt through a large acquisition.

- A correction phase could continue, with impacts spreading to viewers, employees, and investors alike—such as dividend cuts, workforce reductions, and asset sales.

#### REITs/Real Estate (Real Estate -5.87%)

- Concerns over rising interest rates are also negative for real estate and REITs.

- That's because rents can't be raised much immediately, while loan interest and funding costs rise right away.

- The data center REIT Equinix (EQIX) held up at +2.34%, but the overall sector was crushed by the interest rate burden.

---

### 5. Healthcare/Utilities/Industrials: Even "Safe Assets" Were Not a Perfect Refuge

- Healthcare (Healthcare -4.61%)

- Centene (CNC) plunged about -21%, increasing volatility within the sector.

- Uncertainty over reimbursement rates and regulations related to US government healthcare programs (Medicaid, Obamacare, Medicare Advantage), which has persisted over the past several months, was highlighted again, heightening caution toward insurers heavily dependent on the government.(reddit.com)

- It's another case showing the risk that if the government judges it is "giving insurers too much," a single line of policy could greatly shake insurers' profitability.

- Utilities (Utilities -4.42%)

- Usually, when the market is uneasy, money flows into utility stocks (electric/gas companies) with stable dividends, but this time they actually fell sharply due to interest rate rise concerns.

- The reason: Utilities carry a lot of debt and have relatively low profit growth rates, so when Treasury yields rise, the judgment becomes "there's less reason to take risks and buy utilities."

- Industrials (Industrials -5.41%)

- Some stocks like GE Vernova (GEV) and Delta Air Lines (DAL) were positive, but the sector as a whole faced the dual pressure of economic slowdown fears + rising fuel costs.

---

## Flow Seen Through Multiple Timeframes: Trend Extension vs. Pullback

As the table shows:

- 10D: Only 1 of 11 (energy) was positive

- 30D: Only 2 were positive (including energy)

- 120D: 7 were positive, with energy strongest at +31.17% and communication weakest at -8.92%

To summarize:

1. Energy: Strong across 120D → 30D → 10D

- A clear continuation of the uptrend. While caution is warranted for volatility from short-term surges, the structural bullish logic holds as long as inflation and geopolitical risks continue.

2. Technology/Communication: Still positive or weakly negative over the mid-to-long term (120D), but with 30D/10D performance slowing or reversing

- The "AI/Big Tech long-term growth" story is alive, but it appears a correction is underway in the segments where prices had risen too high.

3. Financials/REITs/Consumer: Negative or weak across both 30D and 120D

- As representative sectors hurt in an era of high rates and debt burdens, this week's decline also appears to be an extension of the existing downtrend.

---

## Final Session (24H): "A Small Breather Amid Fear"

- On a 24-hour (most recent trading day) basis, only financials were slightly positive (+0.08%), and all other 10 sectors fell.

- In particular, utilities -3.78% and REITs -2.99% indicated a "cash preference" period where selling spread even to conservative sectors.

- However, rather than placing great significance on a single day's data itself, it's better to interpret it as "investors are still not confident about direction and are moving defensively."

---

## Points to Watch Next Week: 3 Things Individual Investors Should Check

1. The Direction of Oil and Interest Rates

- If oil prices keep holding in the $90–100 range or rise further, the story of inflation and renewed rate increases could grow stronger.

- Conversely, if oil takes a breather and Treasury yields stabilize, there's room for a relief rally in growth and consumer stocks.

2. Regulatory/Investigation News Related to AI/Digital Infrastructure

- As in the SMCI case, this is a period where "policy/regulatory risk" becomes a key variable for growth stocks.

- It's necessary to also watch export controls, accounting issues, and antitrust investigations of companies with similar business models.

3. Checking Heavily Indebted Companies and High-Dividend Stocks

- Companies that rely on large acquisitions and high leverage (borrowing) like PSKY,

- And sectors like utilities/REITs that pay high dividends but have low growth and heavy debt,

- Are candidates whose price corrections could last longer if the interest rate environment stays tight longer than expected.

To summarize, this week's market was "a week where only energy smiled while the rest stayed tense."

Next week, oil prices, Treasury yields, and regulatory news related to the AI/media sectors are likely to drive investor sentiment.

This content is written for informational purposes only and does not recommend investment in any specific stock or asset.

Source: https://nextinvest.org/ko