Second week of June sector summary - 'Tech takes a breather, REITs and defensive stocks rise' amid interest rate and inflation concerns

June 14, 2026 Weekly Market Analysis

## This week's key theme: Sector rotation amid inflation and interest rate concerns

This week (June 8-12, local time), the US stock market was characterized by "reducing some expensive growth stocks (especially tech) and shifting to dividend and defensive sectors."

- On Tuesday (10th), consumer price index (CPI) surprises and concerns about inflation re-acceleration and further tightening emerged, leading to a significant adjustment in tech stocks. In particular, AI server, semiconductor stocks, and super microcomputers (SMCI) plummeted, dragging down the Nasdaq. (www2.stockmarketwatch.com)

- At the same time, tensions in the Middle East (US-Iran) and oil price instability, along with the issue of "raising cash for participation in future mega IPOs (SpaceX, big tech/AI companies listing)" further accelerated profit-taking in high-valued tech stocks. (finance.yahoo.com)

- On the other hand, REITs (Real Estate) and dividend/defensive sectors (financials, consumer staples, utilities, healthcare) saw inflows of capital. As the US Treasury bond yield stopped its upward trend and took a breather, rotation towards relatively less rising sectors and undervalued dividend stocks intensified.

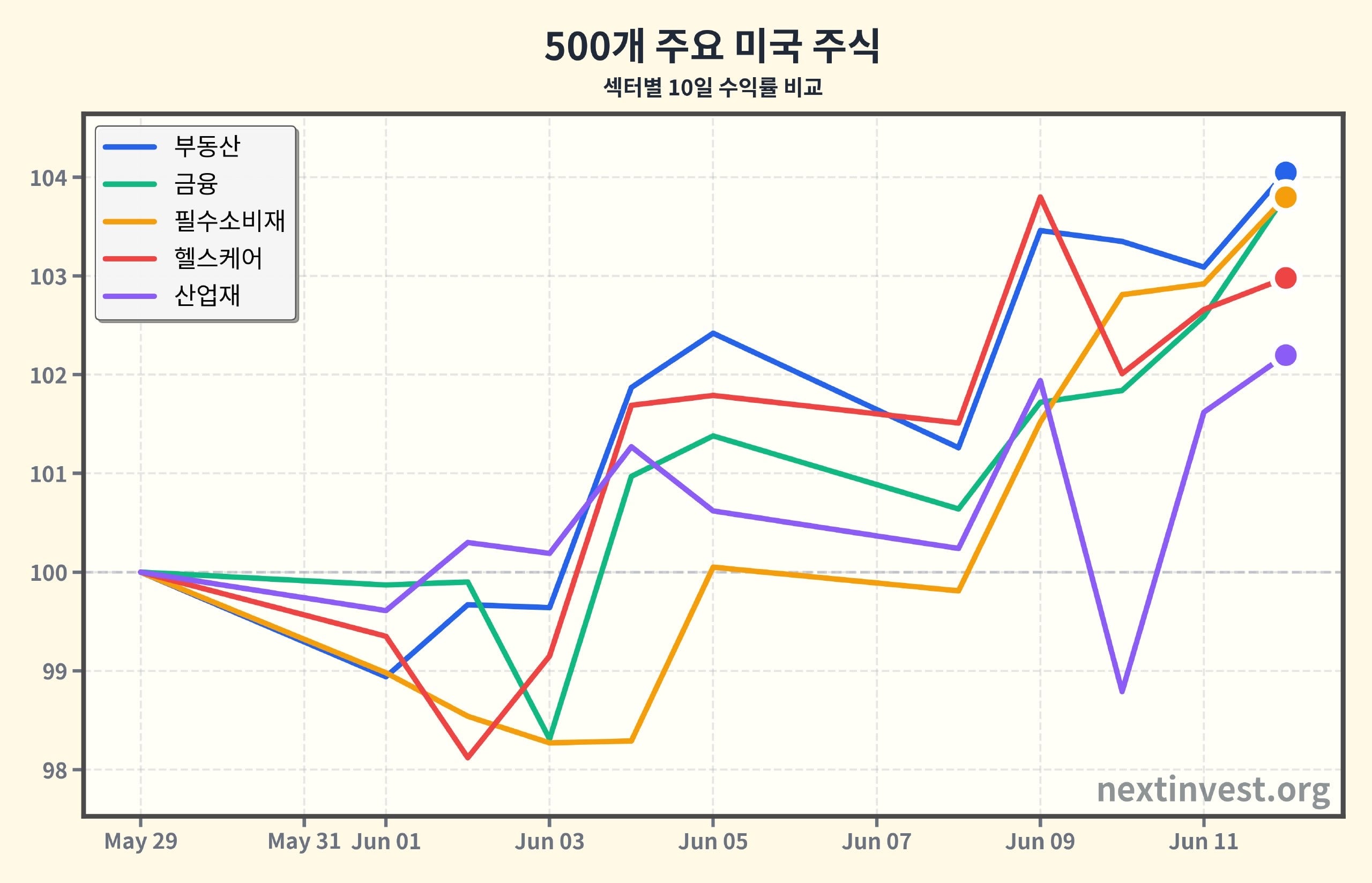

Looking at sector trend data, the technology sector surged by over 40% since mid-March (120D +41.40%) but has adjusted -2.88% in the past 10 days, entering a "breathing" phase within its strong upward trend. Conversely, REITs and financials, consumer staples have been steadily rising since May and June, ranking among the top performers this week.

---

## Sector Performance: REITs, Financials and Defensive Stocks Strong, Tech and Communications Weak

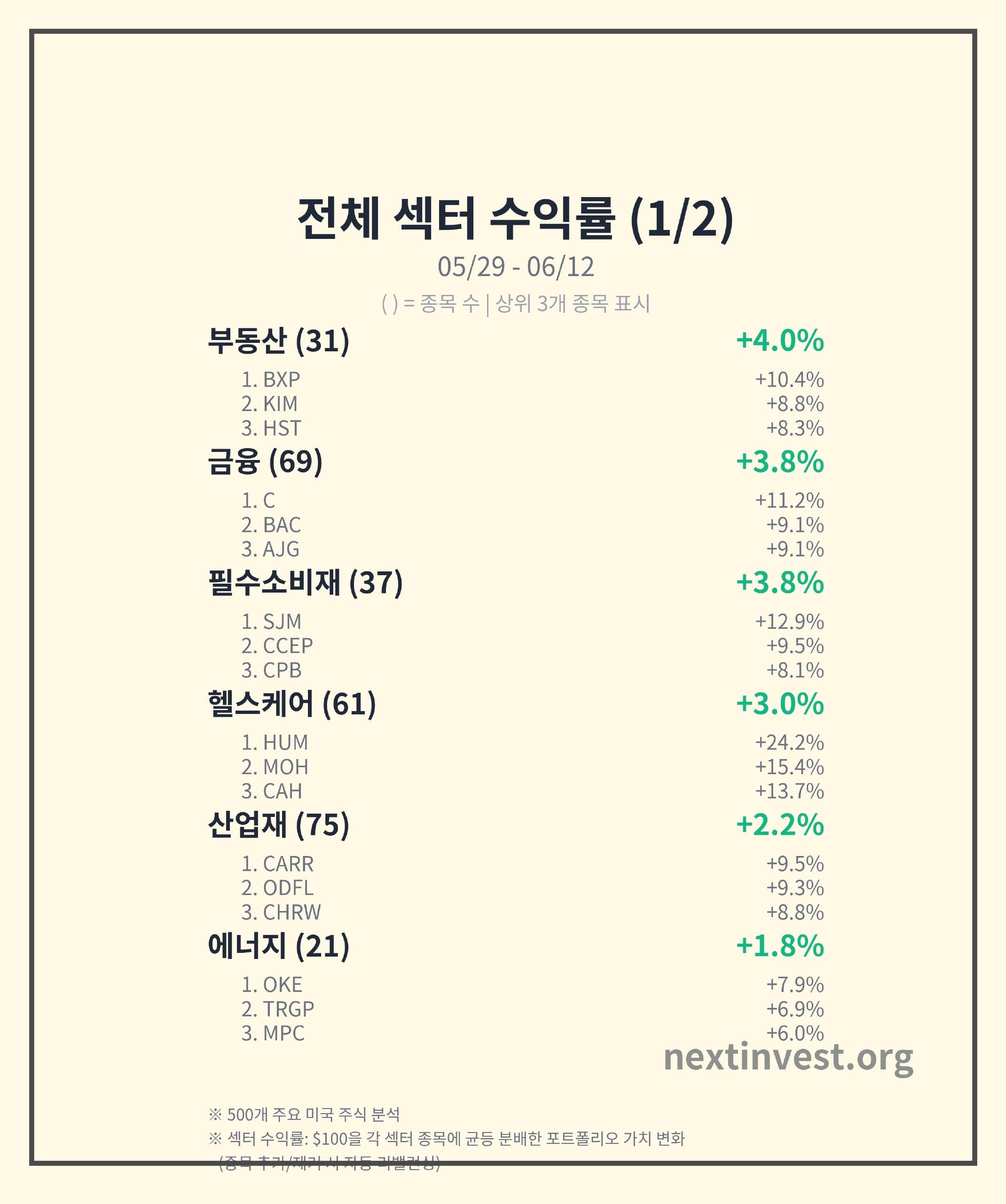

### 1) Real Estate – Most Sensitive to Interest Rate Stabilization

- 10D Return (10D): +4.05% (1st out of 11)

- Representative Stocks: BXP(+10.45%), KIM(+8.77%), HST(+8.31%)

REITs and real estate stocks are "the most sensitive sector to interest rate declines." As the US 10-year Treasury yield peaked (in the 4.5% range) and stabilized over the past few weeks, buying sentiment flowed into undervalued REITs. Some reports analyze that "funds exiting well-performing tech are moving into REITs." (unitedstatesrealestateinvestor.com)

Looking at sector trend data:

- After a -3.8% adjustment at the end of March, it continued to rise gradually throughout April and May. Since June 3rd, it has entered a +4.44% upward trend.

- The 30D performance is also +5.15%, and the 120D is +14.08%, showing a steady upward trend in both short and medium term.

What this means

- This reflects the expectation that mortgage interest rates and commercial real estate financing costs may stabilize somewhat.

- With relatively high dividend yields and strong defensive characteristics, it is emerging as a choice for investors seeking "a more stable alternative to tech stocks whose prices have risen significantly."

---

### 2) Financials (Financial Services) – Large Bank Rally, Relief from Interest Rate Level Maintenance

- 10D Return: +3.82% (2nd)

- Representative Stocks: Citigroup(C, +11.20%), Bank of America(BAC, +9.14%), Arthur J. Gallagher(AJG, +9.11%)

Financial stocks, including banks, insurance, and brokerages, saw a clear rebound this week.

- Improved performance since the first quarter, stable capital ratios, and the issuance of recently issued interest rate-linked and fixed-rate hybrid bonds (coco bond characteristics) offering relatively high coupons are attracting investor demand. (ubs.com)

- The fact that the interest rate did not fall sharply or rise significantly helped to alleviate some uncertainty about net interest margin (NIM), which was a positive factor.

In terms of sector trends:

- After a slight adjustment in April and May, the current upward trend started on June 3rd, recovering about +5.6% and changing the atmosphere.

- The 30D performance is +2.76%, which is still not strong enough to be called a bull market, but it can be seen as a "flow of bottoming out and rebounding."

From a living and investment perspective

- The strength of bank stocks can be interpreted as a sign that credit crisis concerns are not significant, and that lending and consumption activities are holding up to some extent.

- However, some large banks also face regulatory and investigation issues (e.g., investigations related to the "debanking" of specific accounts), so while dividends and valuations are positive, it is necessary to check individual issue risks. (reddit.com)

---

### 3) Consumer Staples·Healthcare – The Role of "Cash Refuge" in Defensive Sectors

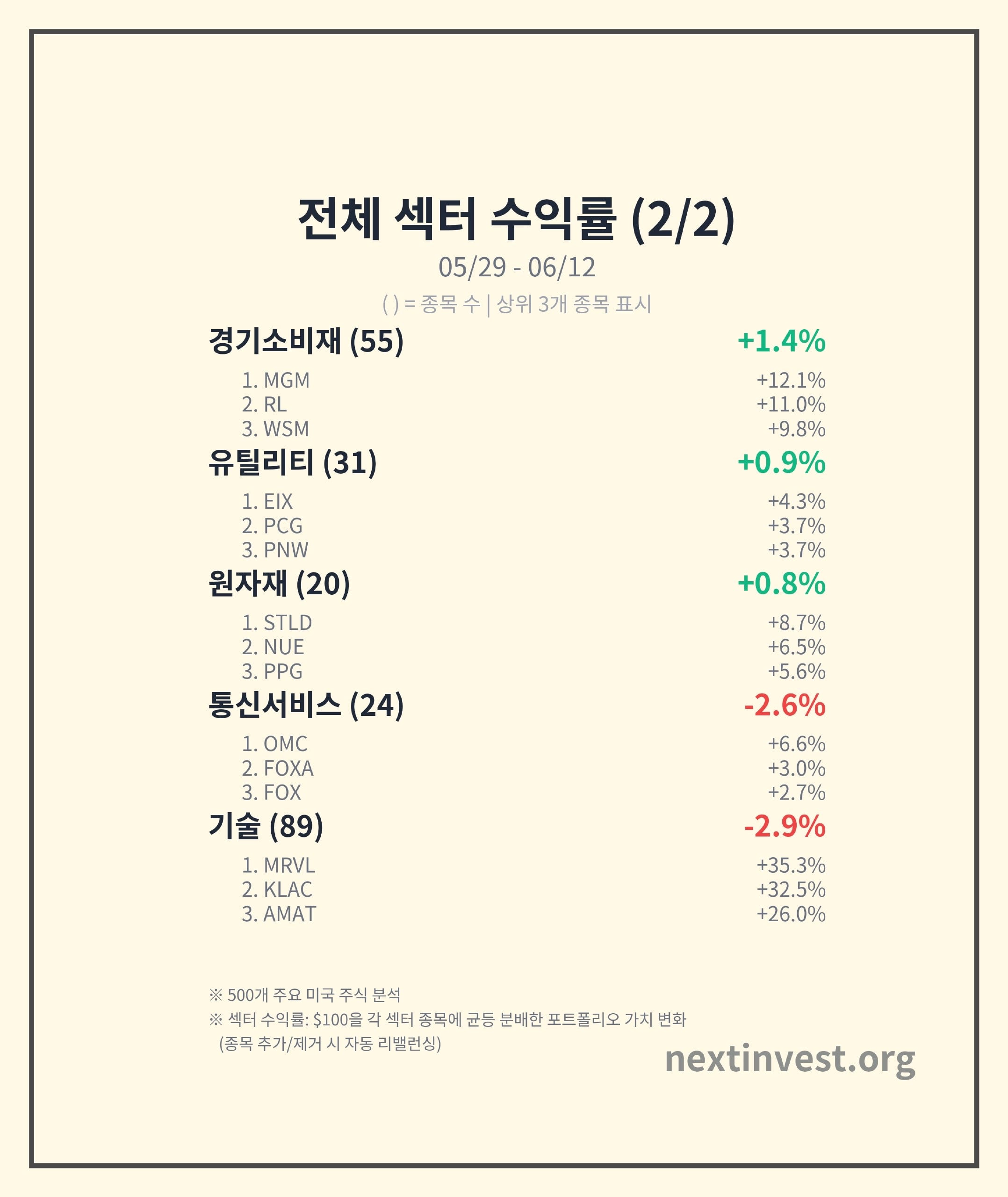

#### Consumer Staples (Consumer Defensive)

- 10D Return: +3.80% (3rd place)

- Representative Stocks: SJM(+12.88%), CCEP(+9.54%), CPB(+8.05%)

Food and beverage companies, which are consumed regardless of the economy, had a strong week.

- As inflation concerns resurfaced, preference for brand consumer goods with high price pass-through ability increased.

- It is a typical defensive sector that stands out with dividends and stable cash flow when the market shakes.

Sector trends are:

- After a short adjustment at the end of May, it entered a +5.55% rebound zone from June 3rd, which is reflected in this week's 10D performance (+3.80%).

#### Healthcare (Healthcare)

- 10D Return: +2.98%

- Representative Stocks: Humana(HUM, +24.16%), Molina Healthcare(MOH, +15.37%), Cardinal Health(CAH, +13.74%)

Healthcare has policy risks but is structurally less susceptible to demand decline and benefits from an aging population.

- Recently, some insurance, pharmaceutical, and medical device companies have been attracting attention due to issues such as earnings revisions, cost efficiency improvements, dividend/share buyback expansions. (ca.investing.com)

- HUM, MOH, CAH, etc., which already had good momentum, continued to rise in June, leading the sector's return.

Looking at sector trends:

- After a -3.58% adjustment since mid-April, it entered a new upward phase of +5.28% from June 2nd, leading to this week's 10D (+2.98%) performance.

- On a 30D basis, it is +4.11%, and on a 120D basis, it is +0.65%, showing a particularly notable recovery in the past month.

Investor Perspective Points

- As the saying goes, "No matter what happens, you go to the hospital," healthcare can play a role in defending your portfolio during economic slowdowns and interest rate fluctuations.

- However, individual stocks have significant regulatory, litigation, and policy risks, so diversified investment in sector ETFs or large-cap stocks is a realistic approach.

---

### 4) Energy·Industrials·Basic Materials – Mid-Cycle, Volatility Exists but the Trend is Still Alive

#### Energy (Energy)

- 10D Return: +1.76%

- Representative Stocks: OKE(+7.92%), TRGP(+6.87%), MPC(+5.95%)

Oil price volatility increased due to heightened tensions in the Middle East and the possibility of US military action against Iran, with energy stocks once again playing a defensive role. (finance.yahoo.com)

- The 30D return is -4.64%, which means there has been an adjustment period in the past month, but the 120D return is +34.17%, indicating a continued medium-term bullish trend.

- Sector trends have been close to sideways (+0.36%) since May 6th, so this could be a good time to revisit energy stocks.

#### Industrials

- 10D Return: +2.20%

- Representative Stocks: CARR(+9.46%), ODFL(+9.29%), CHRW(+8.82%)

Industrials, a cyclical sector, continued its strong performance as the market view that the US economy would experience a "soft landing" rather than a hard one persisted.

The strength in logistics/transportation and construction/equipment stocks reflects the market's belief that the real economy and global trade are at least not collapsing.

The sector entered a +4.49% rally after mid-May, continuing with this week's performance (+2.20%). On a 120D basis, it is up +11.96%, showing a steady upward trend.

#### Basic Materials

- 10D Return: +0.82%

- Representative Stocks: STLD(+8.69%), NUE(+6.54%), PPG(+5.63%)

Steel and chemicals have already reflected a significant portion of economic recovery expectations with a +21.40% increase over 120D. However, some steel stocks continued to perform well this week.

Expectations for infrastructure investment in China and globally, as well as the reshoring (manufacturing return) theme in the US, are supporting long-term demand stories.

The sector trend has been a gradual rise (+1.22%) since late May, showing a slowdown after a strong 120D performance.

---

### 5) Utilities – 'Bond Proxy' Role Resurfacing

- 10D Return: +0.91%

- Representative Stocks: EIX(+4.30%), PCG(+3.73%), PNW(+3.71%)

Utilities are often compared to dividend stocks and bonds. This week, amid increased volatility in bond yields, the sector saw a renewed appreciation for its fixed cash flows and regulated earnings structure.

The sector entered a +3.62% rally since June 1st, and its 120D performance is also up +7.15%, showing a gradual recovery trend.

---

### 6) Communication Services & Technology – 'AI is Still Hot, but Valuation is a Burden'

#### Communication Services

- 10D Return: -2.58%

- Representative Stocks (Gainers): OMC(+6.59%), FOXA(+3.02%), FOX(+2.67%)

Communication Services, which includes advertising, media, and internet platforms, underperformed overall amid mixed performance from large internet platforms and some media companies.

On a 120D basis, it is down -5.41%, making it the worst-performing sector within the S&P.

The sector trend has been downward (-2.87%) since May 29th, suggesting that "while tech is also under pressure, reopening and advertising recovery stories are not fully compensating for this."

#### Technology – Short-Term Adjustment, but Still the Top Sector on a 120D Basis

- 10D Return: -2.88% (Lowest among 11 sectors)

- Representative Gainers: MRVL(+35.31%), KLAC(+32.55%), AMAT(+26.04%)

- Representative Losers: SMCI(-34.09%) and other AI server and semiconductor stocks

This week, tech experienced a sector-wide adjustment, with extreme "long-short polarization" within the sector.

1. June 10th CPI inflation surprise + Middle East geopolitical risk → Tech and semiconductor stocks broadly declined

- Concerns about inflation resurfaced, along with the possibility of further interest rate hikes, putting pressure on growth stock valuations that have been high for a long time. (www2.stockmarketwatch.com)

- On the same day, SMCI announced a $700 million increase (dilution) and raised funding for a $39 billion AI server order, resulting in a 25~30% drop that significantly shook the sentiment of AI server stocks. (startuphub.ai)

2. AI Semiconductor and Equipment Stocks Rebound Amid Volatility

- Investment in artificial intelligence data centers remains strong, with SOXX (semiconductor index) surging over 2% on some days and leveraged ETFs (SOXL) recording gains of over 7%. (reddit.com)

- AMAT's dividend expansion and increased order expectations due to AI-related equipment investment, as well as KLAC's 10-for-1 stock split and anticipated benefits from AI process control, led to a strong rebound.

3. Sector Trend Perspective

- Still the strongest performing sector within the S&P 500 since March, with a 120D gain of +41.40%.

- However, there was a -10% adjustment between June 2nd and 10th, followed by a rebound of approximately +4.8% after the 10th. Whether this is a "healthy correction" after a short-term surge or a signal of a "peak formation" remains to be seen, depending on future inflation and interest rate data.

Meaning for Investors

- The AI theme remains strong, but the days of "buying anything and everything going up" are likely over.

- It is rational to view this as a period of separating companies with strong growth stories, manageable valuations, capital raising (increases) and regulatory risks from those that do not.

---

## Key Stock Trends: REITs, Large Banks, Healthcare and AI Semiconductors Lead the Week

### REITs and Real Estate: Large Office and Retail REITs Strong

- BXP (Boston Properties): Surged over 10% amid interest rate stabilization and expectations of office REIT valuation recovery.

- KIM (Kimco Realty) and HST (Host Hotels & Resorts) also saw gains of around 8%, reflecting anticipation of interest rate easing and demand recovery for hotels and shopping malls post-reopening.

### Finance: Global Large Banks and Insurance Stocks Rise Together

- Citigroup, Bank of America, etc., saw improved investor sentiment due to expectations of capital policies (dividends and share buybacks) following Q1 earnings releases, as well as demand for recently issued hybrid bonds. (ubs.com)

- AJG (Arthur J. Gallagher) rose over 9% as demand for insurance brokerage and risk management services continued.

### Healthcare: Insurance, Pharmaceutical Wholesale and Managed Care Strong

- Humana (HUM): Surged over 20% as Medicare and Medicaid enrollment growth and medical cost management capabilities came into focus.

- Molina Healthcare (MOH) and Cardinal Health (CAH) also recorded double-digit gains, with expectations of earnings upgrades and structural growth stories regaining attention. (ca.investing.com)

### Tech: SMCI Plunges vs MRVL, KLAC, AMAT Surge, Extreme Polarization

- Super Micro Computer (SMCI): Plummeted over 30% throughout the week due to a large increase announcement and valuation pressure, casting a cold shower on investor sentiment for AI server stocks. (startuphub.ai)

- Marvell (MRVL): Surged over 35% driven by S&P 500 inclusion expectations and AI data center demand, but shows extreme volatility considering the rally in previous weeks. (www2.stockmarketwatch.com)

- KLA (KLAC): Rose over 30% as a 10-for-1 stock split coincided with expectations for increased demand for AI process control equipment. (reddit.com)

- Applied Materials(AMAT): Dividend expansion and increased investment in AI and high-performance semiconductor equipment led to expectations of benefits, resulting in a 20% surge. (reddit.com)

---

## Next Week's Key Points: Inflation, Interest Rates, and the 'Second Act' of AI

1. Additional inflation indicators and the Fed (or Fed member statements)

- Since this week's CPI surprise significantly shook the market, upcoming releases of Producer Price Index (PPI), Personal Consumption Expenditures (PCE) price index, and Fed member statements are likely to elicit strong market reactions.

- Depending on how the narrative around peak interest rates versus further rate hikes unfolds,

- capital flows could shift between tech/growth stocks and REITs/dividend stocks.

2. AI-related earnings, guidance, and capital raising (stock offerings, bond issuances)

- As seen with SMCI, aggressive stock offerings or capital expenditure plans can act as growth engines but may also lead to dilution and volatility for existing shareholders in the short term. (startuphub.ai)

- Future earnings reports, capital expenditure plans, and fundraising methods from AI semiconductor, equipment, and cloud companies could reignite the debate on "qualitative growth vs. overheating" in the AI theme.

3. Real estate and REIT-related indicators and interest rate direction

- Real estate indicators such as housing starts, existing home sales, and commercial real estate loan trends could determine the sustainability of the REIT rally. (spglobal.com)

- Depending on whether the US 10-year Treasury yield hovers around 4.5% or trends higher or lower,

- REITs, utilities, dividend stocks,

- and valuation-sensitive growth stocks (tech) could see diverging future trajectories.

4. Geopolitical risks (Middle East, energy) and energy prices

- News flow related to US-Iran tensions could lead to increased volatility in oil prices and energy stocks. (finance.yahoo.com)

- If energy prices rise sharply again, the pattern of inflation and interest rate concerns leading to tech corrections could repeat.

---

### One-Line Summary

> "This week appears to be the start of a 'breathing rotation' from tech/AI to REITs, financials, and defensive stocks.

> However, the AI investment cycle remains strong, making it increasingly crucial to choose investments wisely."

This content is for informational purposes only and does not constitute investment advice on any specific security or asset.

Source: https://nextinvest.org/ko

Free to share ^^