4/5 Weekly Market Analysis — AI, Gold, and Tired Growth Stocks

April 05, 2026 Weekly Market Analysis

## Key Theme This Week: "AI, Gold, and Tired Growth Stocks"

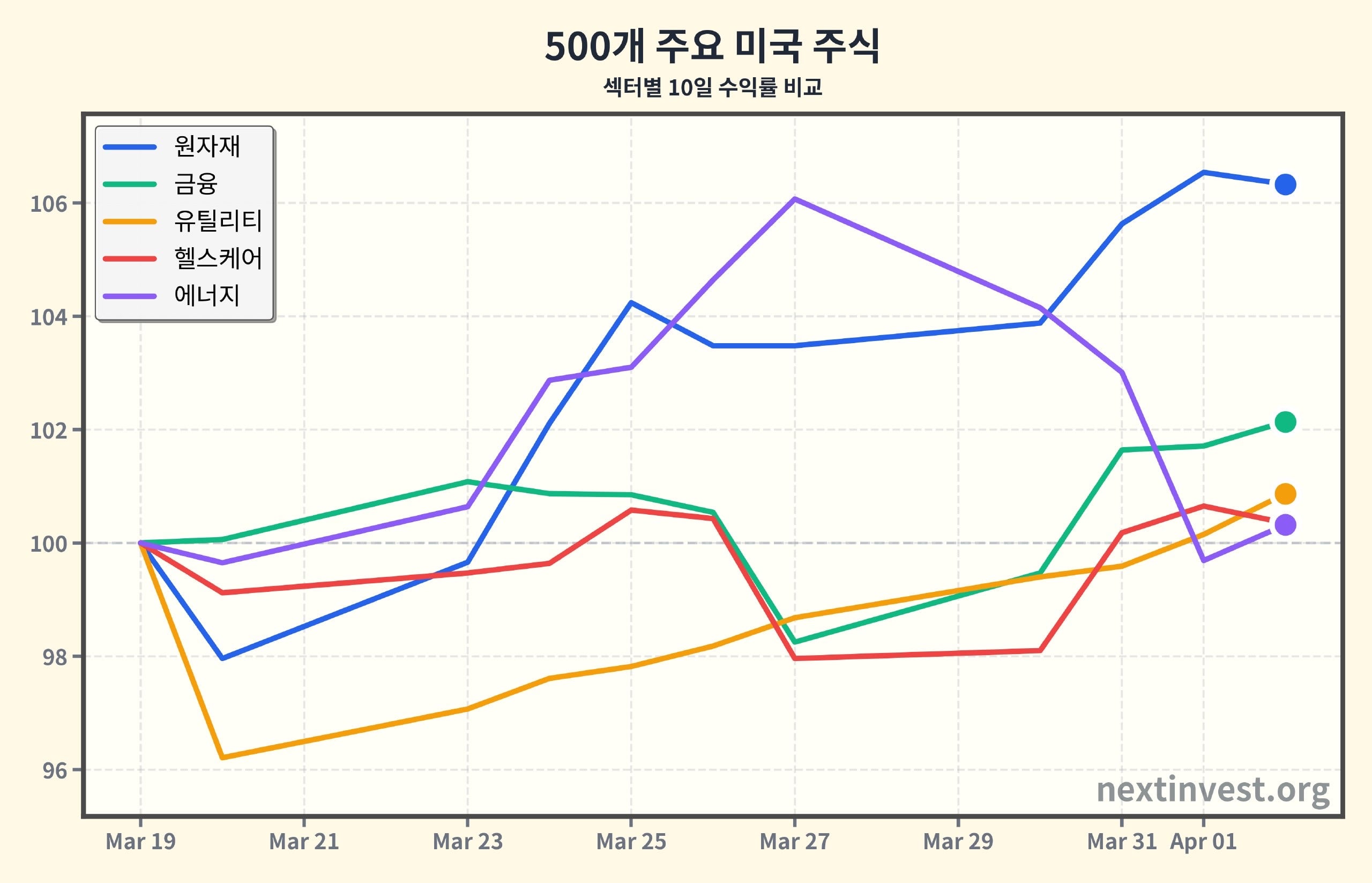

Overall, the U.S. stock market had a rather unpleasant week. Only 5 of the 11 sectors were in positive territory, and the mood across the indices was heavy. But looking beneath the surface, it was a week where the flow of money in and out was clearly divided.

- Technology and some growth stocks took a breather and pulled back,

- Basic Materials and Energy sectors staged a strong rebound, buoyed by rising gold and copper prices.

- Sectors with relatively stable cash flows, such as Financials and Utilities, also drew renewed attention as "defensive plays."

Simply put, people took profits from growth and AI-related stocks that had run up too fast, and rotated some of that money into gold, commodities, and traditional financials.

Looking at the 30-day and 120-day trends:

- Energy is strong on both 30-day (+9.66%) and 120-day (+38.43%) → This week's modest gain (+0.32%) reflects a continuation of the existing uptrend.

- Technology shows negative returns on both 30-day (-1.65%) and 10-day (-1.13%) → A short-term correction phase continues.

- Basic Materials had been largely flat on a 30-day basis (+0.33%) despite strong 120-day performance (+25.00%), but this week's sharp 10-day rebound (+6.33%) suggests the upside trend has been reactivated.

---

## Sector Performance: Who Made Money, and Who Lost It

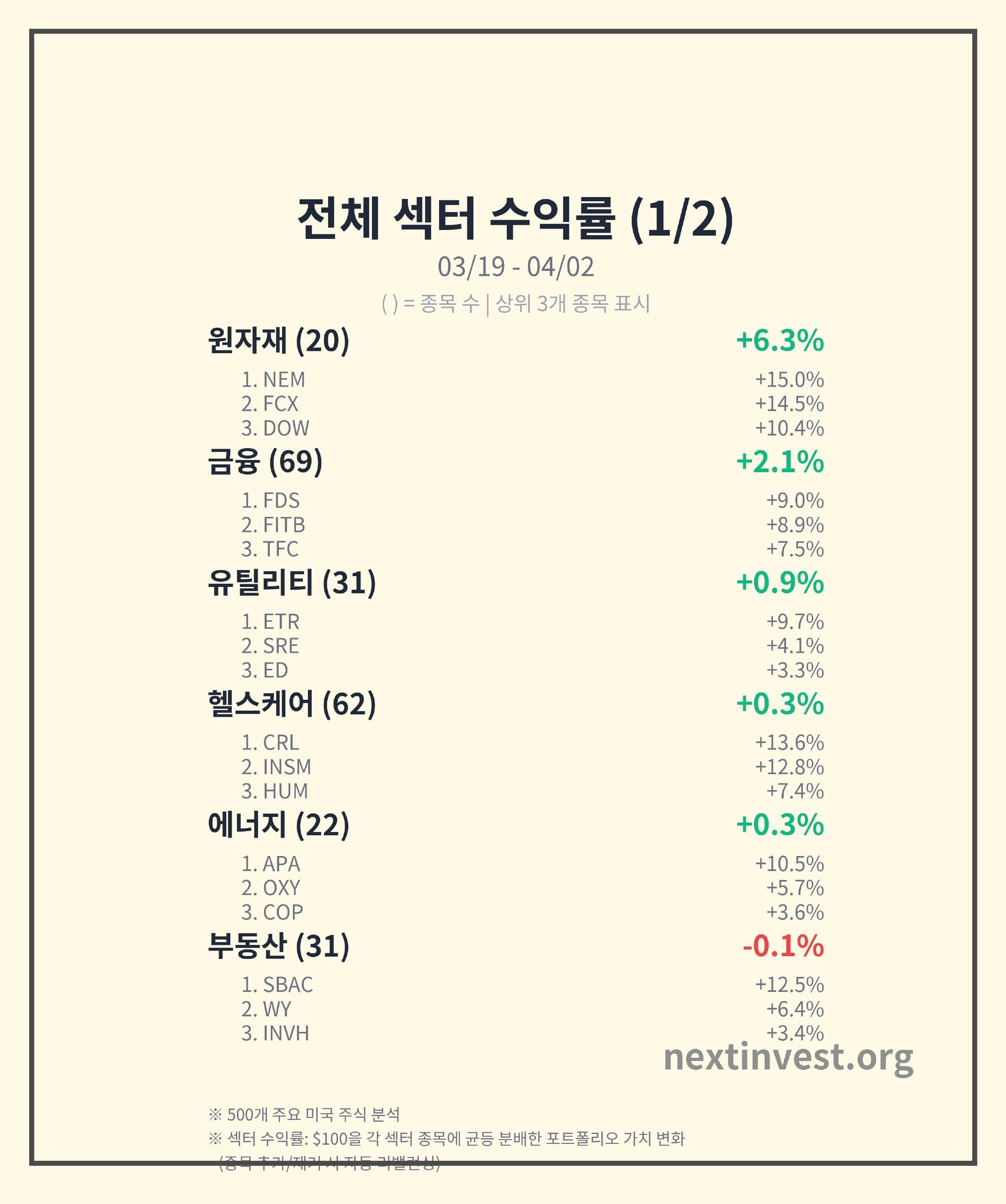

### 1) Basic Materials: Gold and Copper Shine Again

- 10-day return: +6.33% (1st out of 11)

- Notable stocks: Newmont (NEM) +14.97%, Freeport-McMoRan (FCX) +14.47%, Dow (DOW) +10.43%

The strength in the Basic Materials sector this week was driven by rising gold and copper prices.

- Gold prices have continued to rally over recent weeks as renewed safe-haven demand emerges amid inflation and geopolitical risk concerns. Gold miner Newmont (NEM) has been a major beneficiary, posting strong gains for two consecutive weeks. (stoxcraft.com)

- Freeport-McMoRan (FCX) benefited from both rising copper prices and long-term demand expectations driven by expanding EV and data center investment. Copper is an essential metal for wiring, batteries, and data center infrastructure, and is increasingly being treated as a "hidden infrastructure metal of the AI era."

Why does this matter?

- Rising gold and copper prices signal that expectations and anxieties around economic conditions, inflation, and infrastructure investment are simultaneously intensifying.

- Gold-related stocks serve as a "shelter in times of risk," while copper-related stocks act as a "thermometer for economic and infrastructure recovery." The strength in Basic Materials therefore suggests that market sentiment isn't tilting purely toward "fear," but is simultaneously keeping an eye on future growth stories.

---

### 2) Financial Services: Eyes on "Earnings" Amid Peak Rate Debate

- 10-day return: +2.14% (2nd place)

- Notable stocks: FactSet (FDS) +9.02%, Fifth Third (FITB) +8.87%, Truist (TFC) +7.47%

Financial stocks are a sector that makes money from the spread between lending rates and deposit rates.

- Recently, the bond market has been engaged in an intense guessing game over "how quickly and how deeply rate cuts will come." As the gap between short- and long-term rates narrows and expectations of a "soft landing" (a gradual economic slowdown without a sharp downturn) are maintained, regional banks and large regional lenders have staged a relief rally.

- Companies like FactSet (FDS), which provide financial data and research, benefit structurally from increased demand for research and data from institutional investors when market volatility rises — and they have been benefiting from the recent increase in volatility.

Key Point:

- The strength in financial stocks reflects investors' view that they are placing more weight on future earnings recovery than on immediate financial system risk.

- However, on a 30-day basis, Financials (-4.08%) is still underperforming, so this week's 10-day rebound looks less like a "full-blown trend reversal" and more like "excessive pessimism being unwound + some bottom-fishing."

---

### 3) Utilities, Energy, and Defensives: "Seatbelts" in a Volatile Market

Utilities — 10-day +0.87%

- These are companies providing essential public services such as electricity, gas, and water.

- Because demand remains relatively stable regardless of economic conditions, they are favored as a "defensive sector to hold through uncertainty while collecting dividends."

- Capital flowed into representative dividend and regulated-industry stocks, including Entergy (ETR) +9.68%, Sempra (SRE), and Consolidated Edison (ED).

Energy — 10-day +0.32%, 30-day +9.66%, 120-day +38.43%

- APA, Occidental (OXY), and ConocoPhillips (COP) rose 3–10%.

- The backdrop includes oil price strength driven by production management (output cuts) among oil-producing nations and ongoing geopolitical risks.

- Already up more than +38% on a 120-day basis, this week's move looks more like a "breathing-room" gain that maintains the trend rather than a breakout.

Why does this matter?

- Strength in Energy and Utilities reflects the simultaneous pricing-in of "economic slowdown concerns + inflation and geopolitical risks."

- For ordinary investors, this can be read as a signal that the strategy of keeping some defensive sectors in the portfolio to reduce volatility remains valid.

---

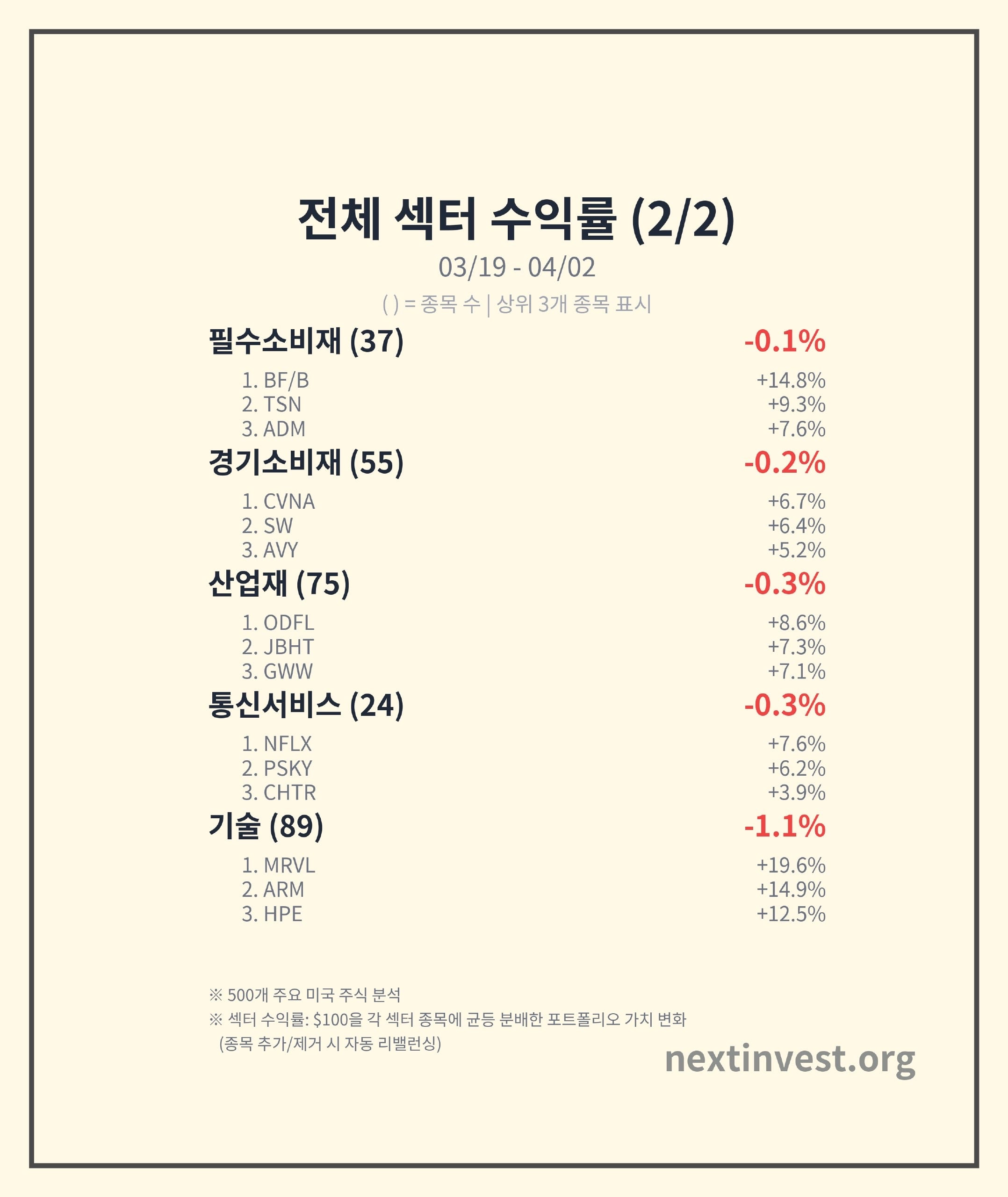

### 4) Weak Sectors: Tech and Consumer-Related Stocks Show Post-Rally Fatigue

#### Technology: -1.13% (Last place out of 11)

- Notable gainers: Marvell Tech (MRVL) +19.64%, ARM +14.86%, HPE +12.45%

- Yet the sector as a whole declined → because sharp drops in a few stocks dragged the whole sector down.

The prime examples are Super Micro Computer (SMCI) and Micron (MU).

1) SMCI -24.59%

- SMCI, once a leading AI server stock, has seen investor sentiment freeze following the indictment and investigation of its co-founder for alleged violations of Nvidia server export regulations, which came to light last month. (tomshardware.com)

- This week, analysis articles and research reports repeatedly highlighted legal risks and governance (corporate transparency) issues, reinforcing the perception that "the growth story is compelling, but the regulatory risk is too great." (investor.wedbush.com)

- Simply put, the label "a company whose technology is great, but where regulations and legal issues could trip it up at any time" has stuck, and investors rushed for the exits.

2) Micron (MU) -17.57%

- Micron reported record-level earnings just two weeks ago, boosted by AI demand, but its share price has since tumbled sharply. (money.mymotherlode.com)

- Selling continued this week amid concerns that Google's announced AI memory efficiency technology ("TurboQuant") could reduce demand for memory chips, as well as ongoing concerns about the burden of large-scale capital expenditure (CapEx) plans over the coming years. (financhill.com)

- In summary, the market has come to the view that "earnings are good, but the stock ran up too much and a lot of investment is still needed, so the share price may need to rest for now."

Influenced by stocks like these, although individual AI beneficiaries continue to appear frequently in the news, the sector as a whole posted negative returns on both the 30-day and 10-day timeframes, making this a week that exposed the fatigue building up in the AI/semiconductor rally.

#### Consumer-Related Sectors: Economic Slowdown and Cost Burden Concerns

- Consumer Defensive: 10-day -0.07%, 30-day -9.18%

- Consumer Cyclical: 10-day -0.17%, 30-day -9.58% (weakest over 30 days)

Estée Lauder (EL) -19.25%

- Estée Lauder, owner of premium cosmetics brands, unsettled investors with news of expanding restructuring costs alongside ongoing reports of negotiations with Spanish beauty group Puig. (stoxcraft.com)

- The concern that near-term costs will increase due to inventory adjustments, store restructuring, and brand portfolio reorganization reflected the worry that "earnings could get worse before they get better."

The broader correction in the consumer sector shows that concerns remain that consumer spending may not be as robust as before amid high interest rates and elevated prices.

---

## Notable Stock Movements: Names That Stood Out This Week

### 1) AI Infrastructure Picks: Why Did Marvell (MRVL), ARM, and HPE Rise?

- Marvell (MRVL) +19.64%

- Marvell, which supplies semiconductors for data centers and communications, staged a strong rebound on expectations of increased AI server investment from cloud companies.

- Recent reports have highlighted that network and storage chips are also essential components of AI infrastructure, and Marvell is establishing itself as a "second-tier AI beneficiary" that is attracting attention later than NVIDIA and AMD.

- ARM +14.86%

- ARM is a low-power chip design (IP) company whose architecture is widely used in smartphones, servers, and automobiles. As power efficiency becomes increasingly important in the AI era, expectations continue to grow that the value of ARM's architecture will increase.

- HPE +12.45%

- HPE, a provider of server and storage solutions, is benefiting from expectations of expanding AI and cloud infrastructure investment by corporations and public institutions.

Key Point:

- Even as the AI boom continues, this week saw the "hottest" names at the forefront (SMCI, some highly valued semiconductors) take a rest, while attention shifted to infrastructure, networking, and low-power design companies standing behind them.

- This kind of movement is commonly described as "money rotating within the same theme."

### 2) Defensive and Infrastructure Plays: Strength in Parts of Telecom, Real Estate, and Industrials

- Communication Services overall was weak at 10-day -0.34%, but individual stocks held up well: Netflix (NFLX) +7.64%, PSKY +6.25%, Charter (CHTR) +3.86%. Streaming, pay TV, and telecom services tend to maintain relatively stable demand regardless of economic fluctuations.

- Real Estate posted a slight decline for the 10-day period (-0.06%), but in the most recent 24-hour session it was the strongest sector at +1.86%. This is the classic pattern in which REITs (real estate investment trusts), cell towers, and logistics warehouses benefit whenever expectations of rate cuts are revived.

- In Industrials, transportation and logistics companies such as ODFL and JBHT rose 7–8%, reflecting expectations of a recovery in domestic U.S. consumer and manufacturing freight volumes.

---

## The Big Picture: What This Week Means Within the 30-Day and 120-Day Trend

- Energy and Materials: Strong on a 120-day basis (+38%, +25%) with additional gains this 10-day period → A signal that the real-asset investment story — inflation, infrastructure, AI data centers — remains valid.

- Technology: Slightly positive on a 120-day basis (+0.61%), but both the 30-day (-1.65%) and 10-day (-1.13%) are negative → Can be viewed as a short-term correction phase continuing after an overheated period.

- Consumer (especially cyclical): Down roughly -9% over 30 days, the weakest of the 11 sectors → A reminder that the burden of interest rates and prices remains a headwind for consumer stocks.

In summary, this can be interpreted as a gradual shift from "a market driven solely by trust in growth stocks and AI" to "a more balanced market that mixes commodities, energy, and defensive stocks."

---

## 24-Hour Snapshot: Sentiment Calms Somewhat Heading Into the Weekend

In the most recent session (24H basis):

- 7 of the 11 sectors were in positive territory,

- Real Estate (+1.86%) led the way, with Utilities, Energy, and Financials also posting modest gains,

- Only Consumer Cyclical (-0.69%) was relatively weak.

This can be seen as a movement toward restoring balance around defensive and dividend sectors, as the anxiety centered on tech and growth stocks during the middle of the week somewhat subsided.

---

## Points to Watch Next Week: What Individual Investors Should Check

1. AI-Related Stocks: The Battle Between "Earnings vs. Valuation (Are Prices Too High?)"

- Stocks like SMCI and Micron, which have strong earnings but face regulatory, investment burden, and valuation issues, can swing sharply on even minor news.

- It is worth continuing to watch where money moves within the AI infrastructure value chain (servers, networking, memory, power, copper, etc.).

2. Interest Rate and Inflation Data

- Depending on the inflation and employment data to be released next week, market expectations about when and by how much the Fed may cut rates could fluctuate significantly.

- This will directly feed into a reassessment of valuations for financial stocks, real estate, and growth stocks (especially tech).

3. Commodity Prices and Energy/Materials Stocks

- If gold, copper, and oil prices continue to show strength, the key question will be whether the outperformance of the Materials and Energy sectors solidifies into a medium-to-long-term trend.

- However, it is also important to keep in mind that a sharp surge in commodity prices can translate into cost pressure (inflation) for the real economy.

4. Guidance (Outlook) from Consumer-Related Companies

- Forward-looking quarterly revenue guidance from sectors such as cosmetics, luxury goods, appliances, and automobiles will provide important clues about actual consumer spending capacity.

- News of restructuring at premium consumer brands like Estée Lauder could be a signal that even high-income consumer spending is not entirely unconstrained.

---

To sum up, this was a week in which gold, copper, energy, and defensive stocks stepped back into the spotlight as the market found it increasingly difficult to push forward on AI and growth stocks alone. For individual investors, now is a good time to review your portfolio and ask yourself: "Am I overconcentrated in a single story? Is my portfolio structured to weather various scenarios — interest rates, commodities, consumer spending, and more?"

This content has been prepared for informational purposes only and does not constitute a recommendation to invest in any specific stock or asset.

Source: https://nextinvest.org/ko