6/5 US Stock Market - "AI Supercycle" Brakes... Tech Stocks Plunge, Investors Seek Refuge in Defensive Stocks

June 05, 2026 Market Analysis

## 1. What Happened Today?

The US stock market saw the first significant slowdown in the "AI·Semiconductor Rally" today.

- S&P 500: Down approximately -2.6%, the worst day since October last year (apnews.com)

- Nasdaq: Down over -4%, the biggest drop since early 2025 (apnews.com)

- Background 1: The US May employment report (non-farm employment) came in almost twice as strong as expected, leading the market to start pricing in the possibility of the Fed raising interest rates again this year. (apnews.com)

- Background 2: Broadcom's disappointing earnings and guidance, which started a few days ago, triggered a reassessment (re-rating) of semiconductor and AI-related stocks, leading to significant selling today. (techpulseglobe.com)

In a nutshell, today was:

> "A hotter-than-expected US economy + overpriced AI·semiconductor stocks = Overheating correction for growth stocks"

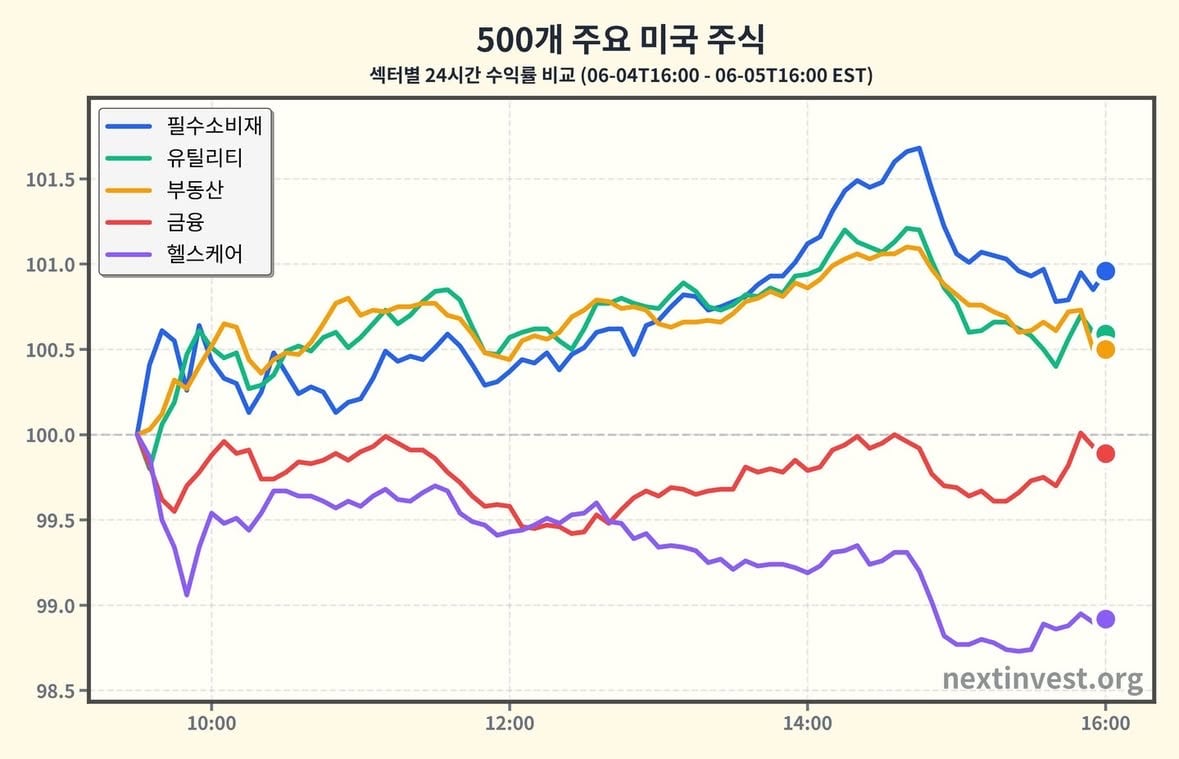

## 2. Sector Performance at a Glance – 'Tech Shock' and 'Defensive Stocks as Safe Havens'

Here's a summary of the 24-hour (June 5th) sector returns you provided:

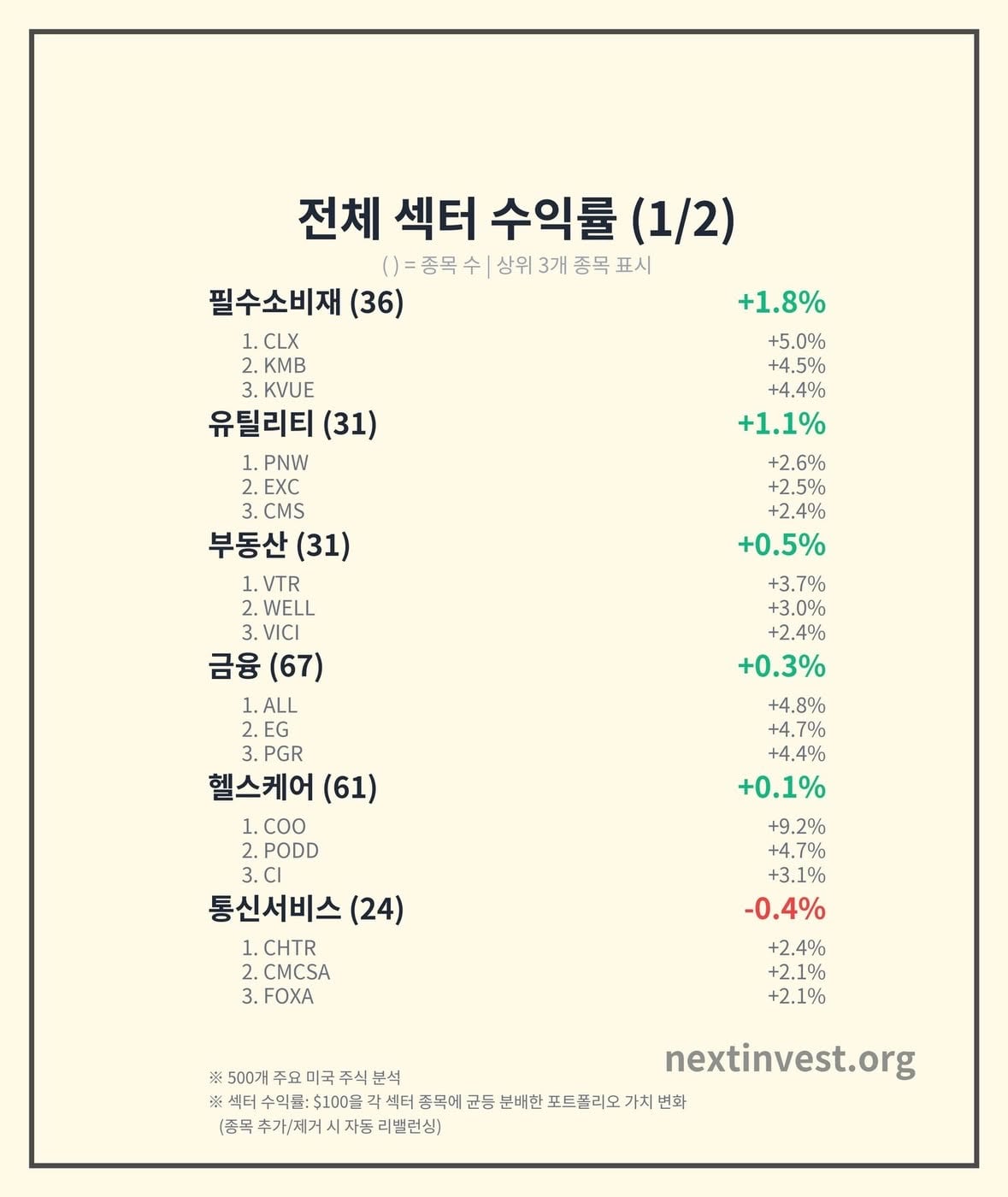

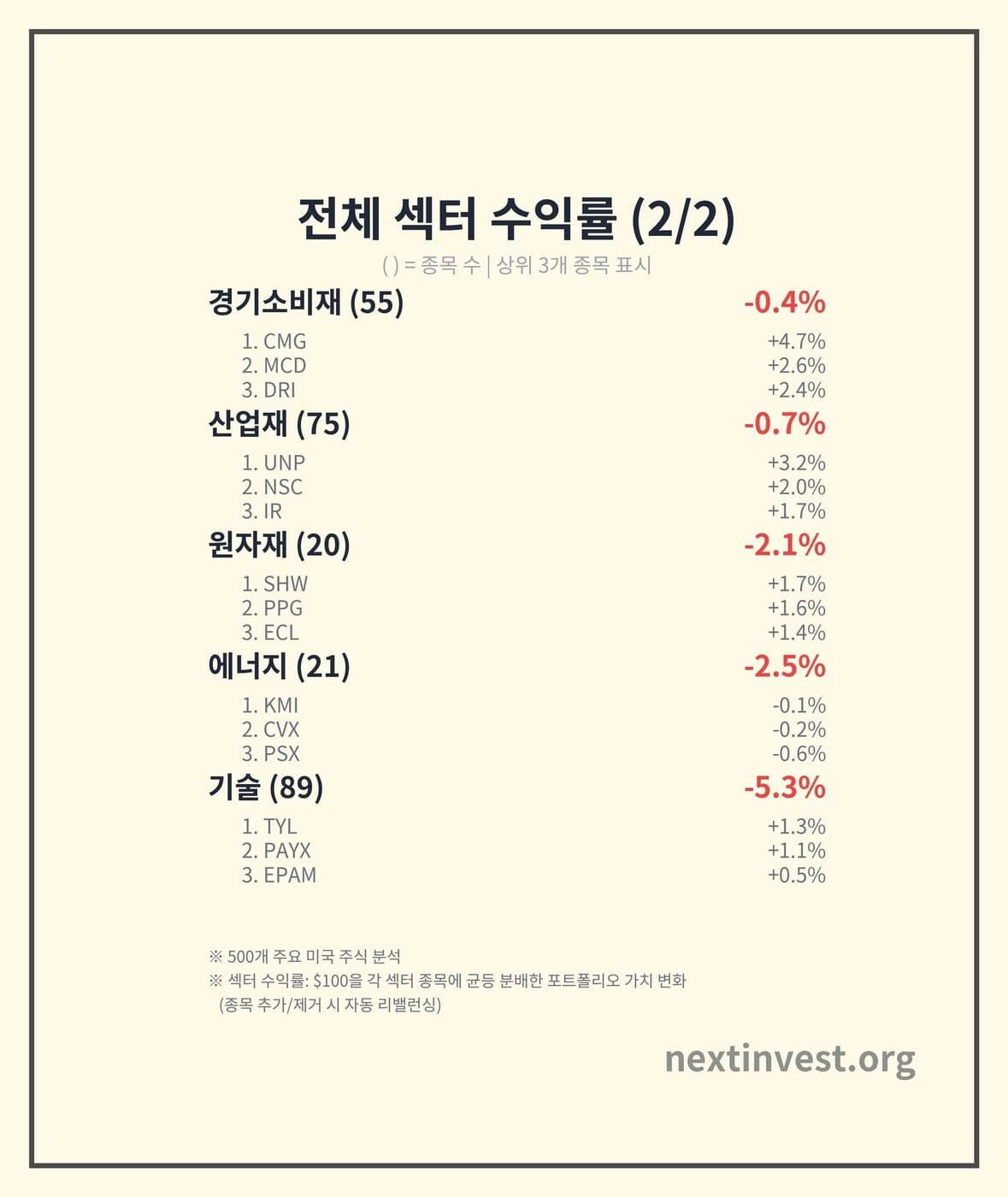

- Technology: -5.27% – Worst performer among 11 sectors

- Energy: -2.48%, Basic Materials: -2.09% – Weakness in cyclical and commodity-sensitive stocks

- Consumer Defensive: +1.76% – Best performer among 11 sectors

- Utilities: +1.10%, Real Estate: +0.55%, Financials, and Healthcare also saw slight gains

This clearly shows a shift from growth and cyclical sectors to defensive sectors (risk-off rotation).

### 2-1. Technology Stocks: The Day the Bill for "Overpriced" AI·Semiconductors Arrived

The main story of today's market was undoubtedly the plunge in technology stocks, particularly those related to semiconductors and AI.

- Estimates suggest that the market capitalization of US-listed semiconductor companies included in the Philadelphia Semiconductor Index evaporated by over $1 trillion in just two days. (uk.marketscreener.com)

- Broadcom's earnings report a few days ago showed that AI networking revenue fell short of expectations, leading to a 13~14% plunge. This ripple effect continued today, dragging down Nvidia, Micron, AMD, Marvell, Arm, and other major AI stocks.

- According to your data, the technology sector was down -5.27% today, with most of the 89 technology stocks declining. The top losers included Marvell (MRVL -17.6%), Arm (ARM -13.6%), Micron (MU -13.4%), Sandisk (SNDK -12.3%), and Qualcomm (QCOM -12.1%), primarily semiconductor and communication chip companies.

Why such a steep drop?

1. Valuation (stock prices) were already too high

- Throughout the first half of this year, "AI infrastructure beneficiaries" have led the index surge driven by the AI boom. The Nasdaq and S&P 500 reached all-time highs in early June, with some semiconductor stocks rising over 50~100% from the beginning of the year. (apnews.com)

- Like Broadcom, even if only slightly disappointing earnings and guidance come out, due to the high stock price level (e.g., P/E ratio of 80x or higher), it had a structure leading to "small disappointment → large stock price adjustment". (techpulseglobe.com)

2. Concerns about interest rate re-increase: 'Most unfavorable news for growth stocks'

- In the May US employment report released this morning, non-farm employment significantly exceeded expectations, shaking the market's scenario of expecting "economic slowdown → interest rate cuts". (apnews.com)

- Bond prices fell (yields rose), and this puts the most pressure on growth stocks (especially high P/E tech stocks) that are sensitive to the present value of future distant profits.

3. Crowd psychology: 'The moment everyone exits through the same door'

- Over the past few months, AI and semiconductors had become almost a common denominator as "must-buy assets", and various quant, ETF, and leveraged products even held the same names.

- In this situation, if one major negative catalyst (Broadcom disappointment, employment surprise → interest rate concerns) emerges, algorithm and passive funds hit the sell button all at once, amplifying volatility. (uk.marketscreener.com)

Based on your 60-day trend data?

- The technology sector had been in a strong medium-term uptrend with over +30% gains since mid-March. From May 19th to June 4th, it rose an additional +15%, essentially being at the center of the "AI supercycle".

- As a result, by portfolio standards, the technology sector still stands at 131.3 from a base of 100 (+31%), with the best performance since the beginning of the year compared to any other sector, but today's -6.6% adjustment marks the beginning of a new downtrend (regime).

What it means to investors

- In the short term, cracks have appeared in the narrative of "AI/Semiconductors = one-way up market".

- However, the medium to long-term trend is still positive, and whether today's adjustment is "cooling off overheating" or the beginning of "bubble collapse" will likely be determined by interest rates and future earnings.

### 2-2. Defensive stocks (Consumer staples, Utilities, Real Estate): "Must eat, use electricity, and own a home"

As growth stocks wavered, money naturally moved to defensive sectors less sensitive to economic cycles.

#### Consumer Staples (Consumer Defensive) +1.76%

- It is the strongest sector today.

- Top gainers: Clorox (CLX +5.0%), Kimberly-Clark (KMB +4.5%), Kenvue (KVUE +4.4%), etc.

- Common point: Companies that sell daily essentials (detergent, hygiene products, basic consumer goods) regardless of economic cycles.

- Strong employment indicators → consumer spending capacity may be fine, but amid interest rate concerns and volatility, "things people continue to buy anyway" appears to be a relatively safe haven.

#### Utilities +1.10%

- As a regulated industry including electricity, gas, and water, it maintains stable demand regardless of economic conditions, so it is frequently mentioned as a "defensive sector" during periods of interest rate uncertainty.

- Today as well, Pinnacle West (PNW +2.6%), Exelon (EXC +2.5%), CMS Energy (CMS +2.4%), and others delivered solid performance compared to the market.

#### Real Estate +0.55%

- Interest rate increases are theoretically negative for real estate, but today seems to highlight "technical rebound from oversold territory + dividend appeal".

- REITs such as Ventas (VTR +3.7%) and Welltower (WELL +3.0%) stood out.

Compared to your medium-term (60-day) trend data

- Consumer Staples: Generally ranging sideways since March, but recently on June 4-5 it stopped its downtrend and shifted to a rebound phase.

- Utilities: Showed weakness (-6% or more) in April-May, and has been in a gradual recovery trend since mid-May.

- Real Estate: Has been on a gradual uptrend since the low point at the end of March, and the pace of gains has accelerated somewhat over the past two days (June 3-5).

What it means to investors

- The market is starting to recognize that "growth stock overheating + interest rate hike risk" are both concerns.

- In terms of portfolio, if the proportion of technology and semiconductors has increased significantly so far, it may be time to consider a strategy to mitigate volatility through the defensive sector.

### 2-3. Finance·Healthcare·Other Sectors: Sectors in the Middle Ground

#### Financials +0.32%

- Generally, interest rate hikes can be positive for banks as they widen the margin between deposits and loans.

- Today, insurance stocks (ALL +4.8%, EG +4.7%, PGR +4.4%) were particularly strong, reflecting a reassessment of investment income and premium increase potential along with rising bond yields.

- Your 60-day trend data also shows that financials have been steadily trending upward since March and have been in a gradual uptrend since May 11th.

#### Healthcare +0.11%

- As a sector with both defensive characteristics and growth stories, it ended slightly positive today amidst overall market volatility.

- The Cooper Companies (COO +9.2%), Insulet (PODD +4.7%), Cigna (CI +3.1%) stood out.

- The 60-day trend has also been gradually trending upward since March, with the uptrend strengthening again in early June.

#### Energy·Basic Materials·Industrials·Cyclical Consumer Goods

- Energy (-2.48%), basic materials (-2.09%), industrials (-0.66%), and cyclical consumer goods (-0.43%) are all sectors sensitive to economic conditions and global demand. Today, when "interest rate hikes → growth slowdown concerns" were highlighted, they generally showed weakness, confirming the pattern.

- Looking at the 7-day trend, energy saw a three-day rally earlier this week followed by a sharp drop today, while basic materials also experienced a gradual rise before a strong bearish candle today. This suggests short-term rallies followed by profit-taking.

## 3. Patterns Revealed When Looking at 7-Day and 60-Day Data Together

Combining the 7-day daily returns + 60-day trend data you provided with today's news reveals the following picture.

1. Technology Stocks

- 7 Days: A sharp rise of +3.6% on June 1st, followed by relatively calm movements for the next three days, and a large adjustment of -5.27% today.

- 60 Days: A strong mid-term uptrend with a +31% rise since mid-March, but today marks the beginning of a new downtrend.

2. Defensive Sectors (Consumer Staples·Utilities)

- 7 Days: A slight downward trend earlier this week, but a clear rebound today alongside the tech stock adjustment.

- 60 Days: No significant upward or sideways movement, but a slight increase in slope since early June.

3. Financials·Healthcare

- 7 Days: Some fluctuations, but relatively stable sectors on a weekly basis including today.

- 60 Days: An upward trend since March, acting as a channel for funds to move from highly valued growth stocks to "classic large-cap stocks with stable earnings."

In summary:

> The "AI·semiconductor concentration bet" that has driven the market for the past two months experienced its first major shakeup today, and this may be one of the first days when some of those funds began to move towards defensive stocks and traditional large-cap stocks.

## 4. From an Individual Investor's Perspective: 'So What Now?'

### (1) Technology·Semiconductors: Should You Fear or Buy the Dip?

- While a drop like today's can be psychologically challenging, it also helps normalize valuations.

- The structural growth story of AI·semiconductors (cloud·data center·edge device expansion, etc.) remains unchanged in the long term. However, the key question is whether the current price reflects this story too excessively.

- If your portfolio has a very high proportion of technology and semiconductors:

- If you have already made significant profits, consider realizing some gains and increasing the proportion of defensive sectors or cash to reduce volatility.

- Conversely, if your technology exposure is low and you believe in the long-term AI growth story, a "phased approach" of gradually buying over several days may be appropriate.

### (2) Defensive Sectors: Rediscovering the Value of "Boring Returns"

- As shown by consumer staples·utilities·healthcare·real estate today,

- While they may not be exciting when the market is doing well,

- It helps reduce the overall decline of the portfolio when the market shakes.

- In particular, companies with relatively high dividend yields and stable cash flows can serve as a middle ground between bonds and stocks in a high-interest rate and volatile market environment.

### (3) Interest Rates and Employment: The Irony of "Good News Becoming Bad News"

- Today's employment data is a signal that the economy is stronger than expected. It's good news if you only look at the real economy.

- However, it also means the Fed may need to keep interest rates high for longer to control inflation, which could be negatively impacting the stock market in the short term.

- Going forward, investors need to keep in mind that "the better the economic indicators, the more headwinds growth stocks may face in the short term."

## 5. Today's Key Takeaways

1. On June 5th, the U.S. stock market recorded its worst day since October of last year due to sharp declines in technology and semiconductor sectors and strong employment data. (apnews.com)

2. Due to disappointing Broadcom earnings and overheated valuations, the technology sector centered on AI and semiconductors faced adjustments of more than -5%, marking the first significant correction to the super rally period of the past two months. (techpulseglobe.com)

3. Some of that capital moved to defensive sectors such as consumer staples, utilities, real estate, and healthcare, which recorded positive returns today.

4. Looking at 7-day and 60-day data together, we can see a larger picture of rotation from short-term overheating in tech stocks to defensive sectors and traditional large-cap stocks.

5. For individual investors, it is now important to adjust the weight of technology stocks, review the weight of defensive sectors, and be aware of sensitivity to interest rates and employment data.

This content is written for informational purposes only and does not recommend investment in any specific stocks or assets.

Source: https://nextinvest.org/ko

You are free to share this without permission ^^